Round One Goes to the Virus

1Q 2020

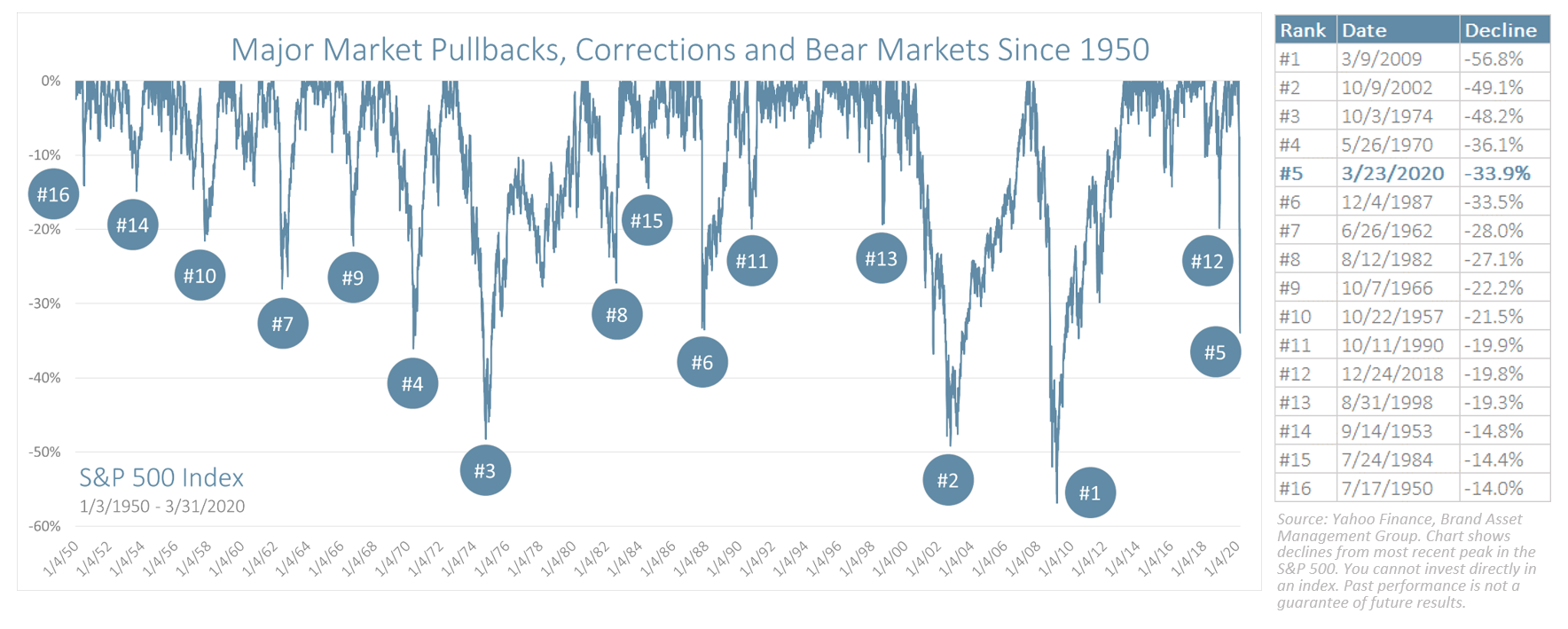

The first quarter of 2020 was a pretty rough one. The S&P 500 ended the quarter down 20.0% (down 19.6% on a total return basis, including dividends) – the worst quarterly return since the fourth quarter of 2008. As everyone knows by now, this was all due to the coronavirus and the toll of this new “war” on the global economy, with a massive decline in oil prices acting as an accelerant. With many instructed to shelter at home, non-essential businesses like restaurants and travel-related companies are finding their revenue streams severely diminished. Many of their employees are being furloughed or laid off. Naturally, with paycheck reductions, most of them are finding the purchase of essential items difficult and any discretionary purchases unthinkable, which is the primary contributor to the economic weakness and the drop in markets.

Bonds played their defensive role in the portfolio for the most part, but as is typical in a “risk-off” environment, “credit” hampered some of the overall effectiveness of bonds. Credit refers to any bond that’s not a US Treasury bond. Because Treasury bonds are generally seen as the safest security in the world, during “risk-off” market periods like the first quarter, investors flock to “safe-haven” assets like Treasuries, driving their values higher and causing interest rates to fall. However, any bonds priced with a credit spread over Treasuries (e.g. agency bonds, mortgage-backed bonds, municipal bonds, corporate bonds, etc.) experienced some decline in price that was generally proportionate to the amount of additional credit risk associated with that bond issuer. For illustration, the Barclays US Treasury Index (one of the best performing bond sectors during the quarter) was +8.2%, while the Barclays US Corporate Bond Index was -3.6%, and the Barclays US Intermediate Aggregate Index (which consists of a variety of Treasury, agency, mortgage-backed, and corporate bonds) was only +2.5% for the quarter. Municipal bonds were also lower, with the Barclays Municipal 1-15 Year Index -0.5% for the period.

To say the first quarter was “rough” for a diversified portfolio is an understatement. If it were a championship boxing match, you could say the judges scored the first round in favor of the daunting contender (the coronavirus) over the defending heavyweight champion (the United States). The good news is, the Champ has been here before. He’s taken big blows early in the match before and ultimately persevered. He’s done the work, studied his opponents, learned from mistakes, and made midmatch adjustments before. That’s why he’s the Champ. Like him, the US has been here before…

In 1942 it looked like the Allies were losing World War II as we were facing supply shortages of critical raw materials for the war effort, higher taxes, higher inflation, and wage and price controls. In October 1962, the Soviet Union had stockpiled nuclear missiles in Cuba capable of attacking the US. In the early 1970’s, OPEC announced they would cease selling oil to the US, resulting in a major energy crisis and a decade of high inflation. In the early 1980’s, Paul Volcker drove interest rates so high to stamp out inflation that we ended up having a savings and loan crisis and a double dip recession. From 2000-2002, we experienced the tech bubble, the 9/11 attacks, and corporate earnings scandals of some of the largest companies in the world (e.g. Enron, WorldCom, Global Crossing), bringing the credibility of the entire stock market into question.

And who could forget 2008 when it looked like the entire financial system would be decimated by a nationwide housing crisis built on overextended borrowers? Somehow, in the face of all those adverse situations, we prevailed and became even stronger in the process.

We are again facing difficult times. We so often hear “it’s different this time”, and it’s tempting to believe that because every new struggle is different. If it were the same as before, it wouldn’t be new and scary, and instead we would hear “we’ve seen this movie before”. To be fair, this one is both different and the same – different in that we’ve never seen a viral pandemic affect the US market in such a way, but the same in that we’ve recovered from even more dire situations.

Recently the White House announced that they project 100,000-240,000 US deaths due to the coronavirus. That’s a huge number, and despite a massive economic stabilization package we’re sure to face some downright ugly economic and healthcare numbers in the coming days, weeks and months. However, it’s important to remember that markets are “discounting mechanisms”, meaning they already take into consideration the collective fear of market participants. So, much of the expected damage caused by this “induced coma” recession may already be baked into expectations. And if the recession is expected to be temporary (which it is), the market will look through that temporary economic valley.

As advisors, our job is to walk through that valley with investors, keep them disciplined and adhering to the plan we helped them develop so they don’t miss the ensuing recovery. Additionally, we strive to create value that regular investors often overlook during such episodes, such as taking advantage of rebalancing and tax loss harvesting opportunities so they can emerge stronger than how they entered the drawdown. The virus delivered some glancing blows in the first round but didn’t knock us down. The judges scored the first round (first quarter) in favor of the virus, but the Champ isn’t done yet. There are 11 more rounds to go, but they may not all be necessary…