A Whirlwind of a Quarter

1Q 2021

It’s fair to say a lot happened in the first quarter of 2021. We began the quarter with a contested election, and then the inauguration of a new administration. The investing lexicon expanded as we experienced our first (but likely not the last) “meme stock craze”. By the end of the quarter, 97.6 million people (according to Our World in Data; nearly 29% of the US population) had received at least one dose of a COVID-19 vaccine – all within about 100 days after the first shot was administered. Many states began opening up and lifting lockdown restrictions, Bitcoin doubled in value, and we blew out candles on the one-year anniversary of the sharpest/shortest bear market in the stock market’s history. And we’d be remiss not to mention the passing of a $1.9 trillion fiscal stimulus package. That covers most of the highlights.

But beyond all those headlines, many important narratives continued to unfold. The US unemployment rate, which had been as high as 14.8% in April of last year, continued to improve, falling from 6.7% in December to 6.0% in March. While that sounds low, we remain encouraged by the fact there is still plenty of room for improvement to get back to the pre-pandemic low of 3.5%. Interest rates continued to rise with the 10-year Treasury more than tripling from its low of 0.52% in August of last year to 1.74% as of March 31st. Many economists and market strategists attribute this move to a higher anticipated growth rate in the economy as vaccinations trend higher and more states begin to loosen restrictions, though some suggest the rise in rates are due to rising inflation.

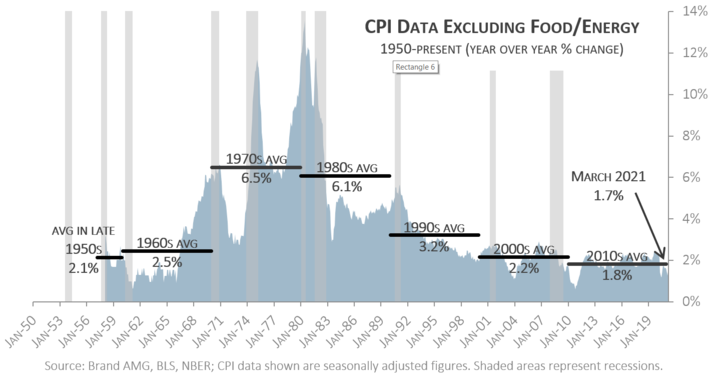

On the topic of inflation, while some are sounding warning bells, others argue that what we are seeing now is temporary and there are plenty of structural forces in place (e.g. technology, demographics, global supply chains) that will continue to keep a relative lid on inflation. For context, we would note that we are not talking about runaway inflation here – the March 2021 Core Consumer Price Index figure (aka Core CPI, which excludes notoriously volatile data like food and energy which can make interpretation of short-term data “noisy”) was +1.7% year-over-year – far from the double-digit levels of the 1970s and early 1980s. Furthermore, we would note the March reading is pushed higher by what is called an “easy comp” – meaning the March 2021 year-over-year reading is being compared to year-ago data that was falling rather quickly. This “smaller base effect” (i.e. denominator) naturally pushes today’s relative reading higher. Because this easy comp effect only gets more pronounced into the months of April, May and June (when Core CPI bottomed), we expect to hear talk of inflation well into the summer.

Amid the backdrop of an improving response to the pandemic, global stocks had a great quarter. US large cap stocks (represented by the S&P 500 Index) were +6.2% including dividends, while smaller US companies performed twice as well – mid cap stocks (S&P Midcap 400) were +13.5% and small cap stocks (Russell 2000) were +12.7%. We continued to see value stocks outperform growth stocks for the second quarter in a row. Among large cap companies, value stocks (Russell 1000 Value) were +11.3% during the quarter, while growth stocks (Russell 1000 Growth) were +0.9%. International large cap stocks (MSCI EAFE) were +3.5%, while small cap stocks (MSCI EAFE Small Cap) were +4.5% and emerging market stocks (MSCI Emerging Markets) were +2.3%. Global real estate was +6.2% for the quarter. The rise in interest rates hurt intermediate and longer-term bonds (because bond prices move inversely to interest rates), causing the Bloomberg Barclays US Aggregate Bond Index to end the quarter -3.4%.

While we are grateful for the returns that the market has given investors over the past quarter (and especially over the last 12 months), we acknowledge investors’ concerns about a market at all-time highs amid a tentative and evolving economic landscape. We encourage investors to remain diversified and note that the evidence shows that disciplined long-term investors are rewarded more than those who attempt to time the markets. Market pullbacks are inevitable, but by augmenting discipline with rebalancing and tax loss harvesting (where appropriate), investors are able to improve their outcomes over time.