The Year of Pandemic-Provoked Persistent Pricing Pressures

4Q 2021

The year 2021 was one of persistent optimism. It began with the hope the pandemic would wane and the world would look more normal by the end of the year. Although we’ve continued to make good progress toward that goal, COVID remains stubbornly persistent and fiendishly adaptable. The US stock market was fairly resolute in its march higher, save for a small pullback in September, with 70 new all-time highs during the year (the second-highest figure on record for the S&P 500 since 1956). Investors seem to be increasingly comfortable with the current trajectory of the economy and maintaining focus on the hopefully not-too-distant end of the pandemic.

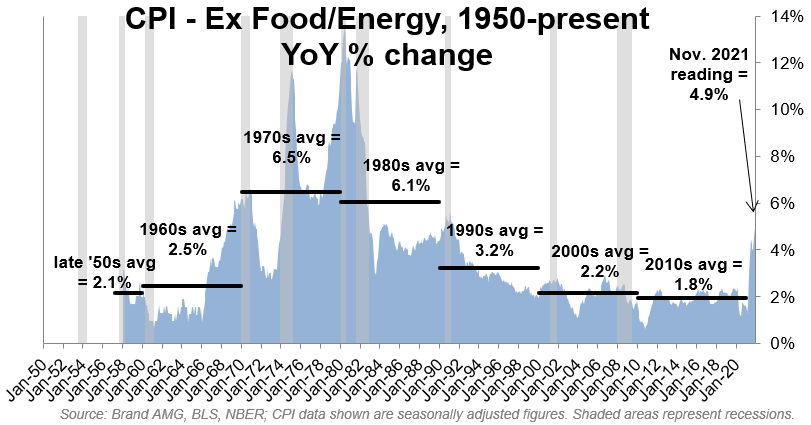

The new storyline on which most market participants have focused is that of inflation – how “transitory” or “persistent” is it? A look at the definition of the word “transitory” indicates that early usage of the word by many economists didn’t necessarily mean a short time frame, but instead was intended to signify that inflation was being caused by temporary factors that would likely self-correct. It was initially thought that the time frame would be rather limited, and so the association between the word and the period of time was assumed. Some of those temporary factors distorting a return to equilibrium were extended unemployment benefits and imbalances in supply and demand. In theory, it was presumed that as we adapted to the virus, workers around the world would return to work, which would increase supply to a level that met that of demand. In practice, there are many reasons workers globally have not returned to work. Tackling those issues ultimately determines the timetable for resolving the imbalance and bringing inflation back down, although we can’t see a return to sub-2% inflation in the near-to-intermediate term.

Acknowledging the stubbornness (“persistence”) of the problem, the Federal Reserve recently stopped using “transitory” in its description of the inflation situation and decided to remove its accommodative policies. We applaud the decision, given that the economy appears to be healing and likely no longer requires the same level of monetary accommodation. The news sent stocks and short-term interest rates higher, flattening the yield curve.

Many of these storylines will likely “persist” into 2022. Hopefully, we continue to make substantial progress against the pandemic, enticing workers back into the workforce, allowing supply chain issues to abate, and alleviating inflationary pressures. If inflation levels fall and the Fed is able to raise interest rates at a measured pace, it could result in further market upside. Furthermore, if productivity gains discovered in the pandemic persist, corporate earnings should remain moderately strong, allowing stocks to “grow into their multiples” without significant disruption to the market.

That said, we know there always exists the opportunity for volatility to rise from out of nowhere. A new variant, an increase of inflation concerns, geopolitical hostilities – any number of negative headlines offer the potential to derail an otherwise optimistic market. It’s important for investors to use opportunities such as those to rebalance and tax loss harvest where appropriate. Because inflation hurts cash and fixed income investments most, it’s also important to make sure investors have the appropriate asset allocation. Now, before volatility pops up, is the time to ensure that the appropriate structures are in place and that investors are prepared to react when (not if) opportunity presents itself. As always, we are here to help guide those discussions.