April Showers…Bring May Flowers?

1Q 2022

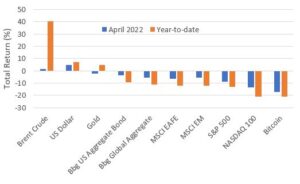

The month of April proved to be a particularly stormy continuation of market volatility, bringing with it negative returns in both the stock and bond markets all around the world. In the United States, the S&P 500 declined over 8.7% and the Bloomberg U.S. Aggregate Bond Index was down almost 3.8%, while the tech-heavy NASDAQ 100 Index was down over 13.3%, its worst single month since October 2008. Through April 30th, there have not been many great options for investing money. Looking at the chart below, sitting in cash might seem like a logical choice, but with headline inflation running at 8.7%, even cash has lost purchasing power.

Source: Morningstar Direct, as of April 28, 2022. Past performance is not indicative of future returns. Investors cannot directly invest in an index.

Several things are contributing to this year’s poor performance including the ongoing crisis in Ukraine, surging inflation, a slowing China, and most importantly, the Federal Reserve as it tightens monetary policy. On May 4, the Fed is expected to raise short-term interest rates 50 basis points to 0.75-1%, and the markets will be looking for signals on the pace of future interest rate hikes. The market currently expects the federal funds rate to end the year at 2.00%-2.25%, which means the Fed would likely raise rates at each of the next six meetings planned in 2022. Fed Chair Jay Powell has been vocal about taming inflation which he has called “much too high” and has said the central bank is committed to raising rates “expeditiously” to bring it down.

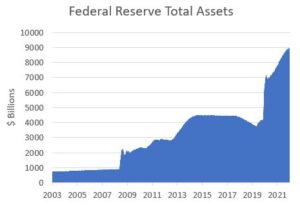

After dropping interest rates to zero during the beginning of the pandemic to help the economy stay afloat, the Fed also began a systematic bond-buying program in June 2020 to keep overall interest rates down. It had been buying $120 billion per month ($80 billion in Treasuries and $40 billion in mortgage-backed securities) until it began tapering in November 2021 and ultimately ending the program in March 2022. This systematic quantitative easing brought the Fed balance sheet up to almost $9 trillion and served to remove much of the volatility around interest rates.

Source: St. Louis Fed, as of April 27, 2022.

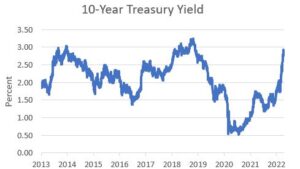

The removal of this program has certainly been felt in the markets but should ultimately be absorbed by other buyers. The last time the Fed “tapered” was in 2014. In that instance, the yield on the 10-Year Treasury jumped from 1.66% to 3.00% in 2013 after then Fed chair Bernanke hinted that tapering would begin in 2014. The yield steadily declined throughout 2014 during the actual tapering, hitting 1.68% by the end of January 2015. This time around, the yield on the 10-Year Treasury similarly rose, almost hitting 3% at the end of April, but it is difficult to say exactly where interest rates will go from here.

Source: St. Louis Fed, as of April 29, 2022.

Raising policy rates raises the cost of borrowing money, which in turn slows growth, leaving the Fed to walk a tight rope to bring inflation back down but not slow the economy down too much. While the U.S. economy did show a surprising contraction in the first quarter, consumer and business spending remains strong, unemployment remains near record lows, and there are no signs that a recession is near. The markets will always produce showers of volatility that can lead to sell-offs, but remaining diversified and taking advantage of buying opportunities (like April) can ultimately produce flowers in our portfolios (hopefully in May).