Time For a Cool Down

By Cliff Aque, CFA

As the summer heats up unseasonably early this year, the Federal Reserve has stepped up its efforts to cool down inflation by raising the Fed Funds rate another 75 basis points on Wednesday, June 15th. The stock market (as measured by the S&P 500 Index), which entered bear market territory at the start of this week, at first reacted positively, but then sold off again on Thursday as investors are concerned about the risks surrounding economic growth… or slowing thereof.

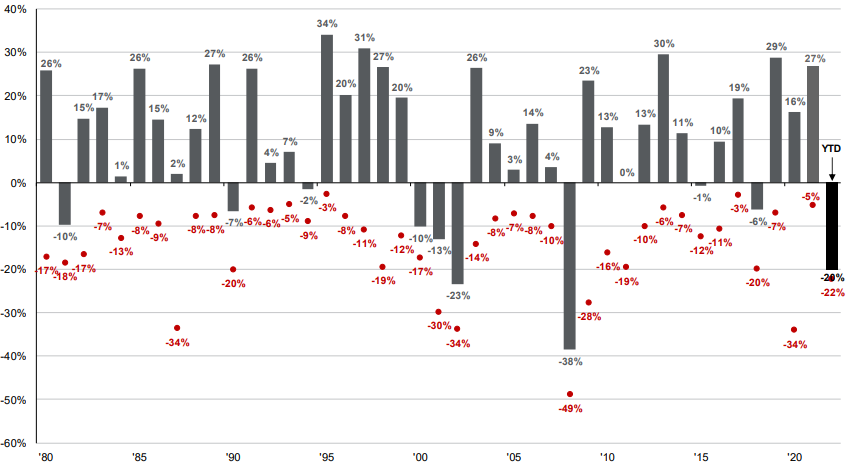

As a reminder, a bear market is declared when a market is down 20% or more from its most recent high. While bear markets are (thankfully) not common, it is important to note that intra-year declines in the S&P 500 Index are not uncommon and have averaged 14% since 1980. However, during that timeframe, the markets have ended the calendar year in positive territory in 32 out of 42 years[1].

It is impossible to say with any certainty where the markets will go from here, but the Fed has clearly stated its intentions to continue raising rates this year. The markets price this information in but can overreact on both the upside and the downside, especially as raising rates increases the chance of a recession. As the Fed walks this tightrope between cooling off inflation while not cooling off the economy too much, markets may continue with elevated volatility.

One thing we do know as patient, disciplined investors, is that it is not time to panic. During downturns like this, aversion to losses may prompt us to consider selling which can often lead to missing a rebound in the markets. The best strategy is to maintain your long-term strategic allocation and rebalance in an effort to buy assets that are low and sell those that are high. This can be especially difficult when markets are volatile and seemingly everything is down, but will ultimately lead us to a better outcome.

It is worth remembering that every single broad market decline from the beginning of publicly traded equity markets to the start of this one has completely recovered and later moved on to new highs. After three good years (2019-2021) in world markets, it should not come as a surprise that “something” triggered this selloff. The inputs of inflation, oil, war and interest rates are certainly valid concerns, but they are certainly not new ones. We will be looking for opportunity and looking forward to talking with you.

[1] Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. data as of 6/15/22. The table above does not depict specific funds, but rather the S&P 500 index. You cannot invest directly in an index. Returns above are price returns, which do not include dividends. Red dots represent largest intra-year declines; grey bars represent calendar year annual returns. Past performance is not a guarantee of future results.