Recap: Focused on the Fed

With heightened inflation and interest rate policy being a focal point for society, our team recently gave a presentation focused on the Federal Reserve (“the Fed”) – a key institution playing a significant role in the response to both challenges. Our discussion focused on the history and purpose of the Fed and the potential implications of current Federal Open Market Committee (“FOMC”) policy. For anyone not able to attend, we wanted to provide additional commentary for your edification.

Brief background and purpose

After failed attempts to establish a central banking system in the 1800’s, the United States was plagued by a fragmented banking system that frequently caused panics and runs. These events had spillover effects on the currency and economy at large, prompting the eventual creation of the Federal Reserve Banking System in 1913. After the Great Depression, the system was further revised in the 1930’s, and the Fed was eventually given its modern “dual mandate” in 1977, which is to maximize employment and to keep prices stable.

To achieve its dual mandate, it will choose to take either an expansionary stance (lower rates, promote growth) or a contractionary stance (raise rates, restrict growth). The main interest rate it aims to influence is the Federal Funds Rate (“FFR”), or the rate that commercial banks use to loan money to each other overnight on an uncollateralized basis. It does this by setting a target range for the rate and then influencing it with a range of tools, which can broadly be classified as traditional tools and nontraditional (or “crisis”) tools.1

Where have we been?

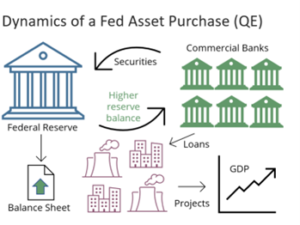

Our discussion focused on the use of quantitative easing (“QE”) – a policy tool first created in response to the Great Financial Crisis (“GFC”). During that time, the FFR was already at zero, and the Fed was unable to positively influence the economy with what was left of its traditional toolkit. The solution? Flood the financial system with liquidity. Within QE, the Fed conducts a series of asset purchases that essentially creates new money in the financial system, while increasing the Fed’s balance sheet.

Source: Microsoft Icons, Brand AMG

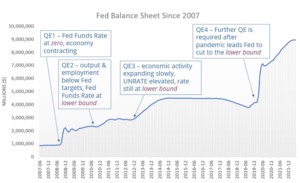

After two rounds of QE in the years following the GFC, the markets had become accustomed to the Fed backstopping the economy. At the beginning of QE3 in 2013, Ben Bernanke announced that the Fed would taper (reduce the level of asset purchases) at some future date. Even the mere thought of future tapering was enough to send the 10-Year Treasury up roughly 100 basis points (1 basis point equals .01%) in 8 months. This period of rising interest rates would become know as “the Taper Tantrum.” 2

At the onset of the pandemic in 2020, the Fed decided to backstop the economy once again with further QE, named QE4. This added even more liquidity to the financial syster (as reflected in the chart below – which is likely a contributing factor to our current levels of inflation.

Source: St. Louis Fed, Brand AMG. Data through 4/30/22

During QE4, fiscal stimulus packages were passed by Congress which created another inflationary factor, this time directly inflationary to the currency.3 With the May inflation (“CPI”) print coming in hot at 8.6% year over year, the FOMC decided to hike the Federal Funds Target Rate by 75 basis points at its June meeting, which was higher than its initial guidance of 50 basis points. In addition, the runoff of QE assets from its balance sheet started on June 1st. All of this begs the question…

Where are we going?

Will the Fed be able to achieve a soft landing for the economy? If you have consumed any financial media in 2022, you have surely heard the term used. Inflation has remained elevated, and the consensus is that the Fed has painted themselves into a corner. To achieve a soft landing, they must cool the economy and return inflation to its long-term average target of 2% while also avoiding a recession and limiting damage to the financial markets. On the opposite side of the coin, if the Fed fails to gently let the economy down and inflation remains elevated, stagflation (high inflation combined with stagnant demand) becomes a concern.

In a complex world, it is a fool’s errand to predict the market’s response based on potential future events. Trying to time the market’s ups & downs can lead to a detrimental effect to the longer-term portfolio returns. While it is emotionally challenging for us all, discipline to an investment structure built around your goals and needs is a major determinant for how quickly a portfolio can recover during a period of volatility. In periods of challenge, the seeds for the next “bull market” are being planted. Companies are finding new ways to meet customer demand and investing in new products, services, and technology to address the needs of the future. To harvest that fruit, staying engaged & disciplined to an investor’s allocation is a major focal point during investing seasons such as this.

Knowledge doesn’t necessarily make it easier, however, and our team is available to connect regarding anything at all.

1Source: federalreserveeducation.org, federalreserve.gov, frbsf.org

2Source: federalreserve.gov, frbsf.org, fred.stlouis.org

3Source: wsj.com, bls.gov, frbsf.org, fred.stlouis.org