Near-Term Turbulence

4Q 2022

By Cliff Aque, CFA

After three consecutive quarters of only mostly negative returns to report, the fourth quarter finally provided positive returns across most asset classes, but not without continued volatility. The downward volatility that marked the second half of the third quarter, continued into the fourth as the S&P 500 Index fell to its low for the year on October 13th. However, things turned around after that point and continued into November as the headline consumer price index (CPI) came down from 8.2% to 7.7% in October and then to 7.1% in November. At this time, there were some “dovish” comments from the Federal Reserve (the Fed), leading investors to once again hope that central banks might become less aggressive with interest rate hikes.

In December, the central banks around the world threw cold water on the global market rally. After the Fed raised rates 50 basis points at its meeting, which the market fully expected, Chairman Jerome Powell gave a comment that was unexpected, saying “it will take substantially more evidence to give confidence that inflation is on a sustained downward path.” The European Central Bank also raised rates and said that more monetary tightening remains, while the Bank of Japan allowed its 10-year bond to move from zero to 50 basis points – its first real move since targeting zero in 2016.

The themes that led to the volatility we saw last year are still with us today. These are high inflation, rising interest rates, the war in Ukraine, Chinese COVID policy, COVID, and a potential recession. After last year’s pullback, much of the bad news we believe to be priced into the market, but we expect the choppy environment to stay with us through at least the first half of 2023. Even in this first week of January we saw the “good news is bad news” theme continue as U.S. jobless claims fell, signaling that the job market is still very strong although this report sent the stock market down.

It is not all bad news though. Remember when you were actually paid to hold cash in a savings account? Even though fixed income investments were down last year, they now offer investors more attractive yields, incentivizing investors to hold them again. If rates continue to go up from where they currently stand there could be some additional losses in store, but the income they pay now helps compensate for that risk. Equity valuations have also corrected to a “reasonable” level, and as of December 31st, the forward price/earnings (P/E) ratio on the S&P 500 Index stood at 16.7, just below its 25-year average of 16.8. Emerging market valuations are also just below their 25-year average P/E while Europe and Japan are even more significantly below their averages. Compared to where we started 2022, the investment landscape is much more attractive in 2023 but we must be prepared for volatility and act accordingly to maintain a long-term view.

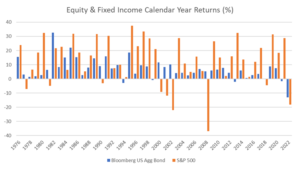

Source: Morningstar Direct, Brand AMG. Investors cannot invest directly in an index. Past performance is no guarantee of future results.

Speaking of the long-term, even with the negative year we just experienced, the S&P 500 is up an annualized 7.7% over the last three years, 9.4% over the last five, and 12.6% over the last ten. While we are not calling for the start of another bull market, it is rare to see two negative years in a row for equities, and even rarer in fixed income. Properly allocated portfolios are designed to be functional and durable in both positive and negative market environments. At present, we often see this occurring intra-week. That isn’t always the case and in balance, we are expectant of better days in 2023 than 2022. Either way, disciplined thought and action will be called for and rewarded.