Short-Term Volatility

By Cliff Aque, AIF®, CFA®

The markets sold off early Monday morning on a myriad of worries including (but not limited to) an over-valuation in some of the largest technology companies, a weak employment report on Friday, fears of an escalation in tensions between Israel and Iran, and an equity sell-off in Japan. We noted in our last quarterly update that the valuations of the largest companies were skewing the valuation of the overall market. While we did not expect a dramatic fall, the reality is that the Nasdaq 100 (generally considered a technology index of the 100 largest companies) had ended each of the last four weeks lower, so a sell-off had already begun.

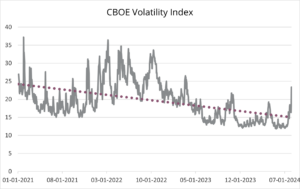

As of this writing, the markets have rebounded off of their lows, but this movement has reawakened market volatility which had been extremely low in recent months. The CBOE Volatility Index, commonly referred to as “VIX,” measures the market’s expected volatility over the next 30 days based on investor activity in options on the S&P 500 Index1 . VIX has been trending steadily down over the last few years and has hovered below 15 for most of 2024. The longer-term average has been slightly above 20, so apart from a brief spike in April, 2024 has been a rather calm year as the broader market climbed steadily higher.

Market drawdowns are not uncommon, especially after considerable returns. Remember that the S&P 500 Index was up over 26% in 2023 and up over 15% in the first half of 2024. Considering the number of uncertainties in the world and the lofty valuations of some of the largest companies, a slight sell-off was probably warranted. Stocks trade based on earnings, and broadly speaking, these are still on solid ground, backed by a relatively sound consumer and a strong employment market (despite weaker numbers last Friday). Investors are best served to ignore short-term volatility and focus on the long-term which is what we do at Brand Asset Management Group. Please do not hesitate to reach out to us with any concerns – that is what we are here for.

1Investors cannot invest directly in an index