Enduring the Dog Days

2Q 2012

The record-setting heat wave that recently took hold over large swaths of the United States has left millions of Americans feeling a little worn out and lethargic. During the second quarter of 2012, despite periodic episodes of both up and down volatility, global markets can be described in an overall similar fashion.

Over the last few months, clouds of uncertainty trapped and intensified that figurative heat worldwide. In several key emerging markets, such as China and India, moderating trends began to impact what’s been persistently remarkable growth. Europe, meanwhile, continued to struggle with broad-based fiscal instability in addition to the near-term effects of mandated austerity measures. Here at home, headwinds in the form of a stagnating jobs recovery and a high degree of political and legislative ambiguity kept a lid on any continuance of the first quarter’s strong results. However, June made up for much of the “bearish” outcomes witnessed in April and May.

EQUITY PERFORMANCE:

U.S. stocks were middling at best this past quarter, with the S&P 500 Index falling 2.75%. Still, year-to-date returns of 9.49% put this modest drop into a less troubling perspective. Internationally, the landscape has been significantly more challenging and quarterly results were clearly soft. That said, the MSCI EAFE Index of developed nations in Europe, Australasia, and the Far East remains up 3.38% for the year, while the Emerging Markets Index has gained a respectable 4.13%. To us, recent weakness has presented an excellent opportunity for rebalancing into international positions at attractive valuations. Global Real Estate, which we classify as part of our alternative investments sleeve, continued to hold up well with a modest quarterly gain of 1.49% to build on a very strong first quarter.

THE FIXED INCOME PICTURE:

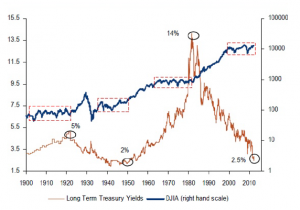

In June, Federal Reserve Chairman Ben Bernanke announced an extension of “Operation Twist” to hopefully encourage long -term investment throughout the economy. With the combination of “risk-off ” trading and further interest rate suppression, bond prices traded higher and the Barclay’s Capital Aggregate Bond Index gained 2.06%. Despite this ongoing performance, fixed income valuations (particularly of U.S. Gov’t issues) in today’s unprecedented interest rate environment are making it simply too expensive to be too conservative. The 10-year Treasury hit a 200+ year record low yield of just 1.45% during the quarter! As we remain focused on achieving the long term financial goals of our clients, we continue to advocate for a disciplined asset allocation plan and robust portfolio diversification.

Though we’ll make no efforts to prognosticate when it might happen, we can reasonably assert that the economic and political heat wave will at some point break, and the financial markets’ own dog days will conclude. Importantly, the first half of this year has actually been quite solid as you’ll see in the statements that follow. To that end, we strongly encourage clients to divert their attention from the noise and prognostication that seems to rival last summer’s and to focus instead on the time-tested principles to which we subscribe. After all, no one has ever been cooled off by talking about the heat.

Chart: Equity Prices And Bond Yield Since 1990 , Monthly data. Source: BofA Merrill Lynch Global Equity Strategy, Bloomberg, Haver