A Crack In The System

1Q 2023

By Cliff Aque, AIF®, CFA®

Another tumultuous quarter is behind us after a banking crisis was added to the mix of worries that still include persistent inflation, continued rising rates, the war in Ukraine, tensions with China, and of course, the looming recession. Overall, performance across most major asset classes was positive during the first quarter, led by large cap growth companies. In our last quarterly update, we said we expected the choppy environment to stay with us through at least the first half of 2023, and we expect that will continue to be the case as investors look for more clarity around the issues mentioned above.

I was installing a light fixture the other week and as I tightened the screw that held the glass enclosure around the lightbulb, I heard (and saw) a crack, and it reminded me of a saying that the Federal Reserve (Fed) always tightens until something breaks – apparently I am not the only bad handyman. After the collapse of several regional banks, which we wrote about here, the market thought that might have been the break the Fed needed to see, but on March 22 the Fed raised the federal funds rate another 25 basis points the next week. Fed Chairman Jerome Powell has made it repeatedly clear that inflation is their priority and that the costs of not bringing inflation down would be worse than the costs of bringing it down. The market seems to be pricing in at least one more interest hike of 25 basis points, but there could be more if inflation does not continue to recede.

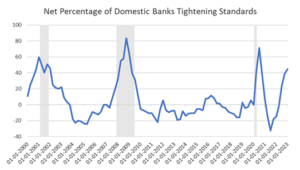

These higher rates and the turmoil in the banking sector are likely to cause lending conditions to become even tighter than they already were, further reducing liquidity in the economy and making a recession more imminent. The charts below show the net percentage of banks tightening standards for commercial and industrial loans to large and middle-market firms as of January and the year-over-year change in the money supply which is now negative for the first time since the late 1940s as of February. These readings are certainly likely to be worse after the bank failures in mid-March.

The labor market continues to be a bright spot, although the unemployment rate finally saw an uptick from 3.4% to 3.6%,[1] but that is off 50-year lows. Businesses are reducing hiring based on lower job openings and increased layoffs, and they are likely to pull back further to offset slower demand and higher costs. However, the unemployment rate is unlikely to climb dramatically because we have a structurally smaller labor force since the pandemic as many workers have left the workforce and “legal” immigration has been low.

Despite some jitters to start the year and plenty to remain concerned about, we encourage investors to stay diversified and take advantage of opportunities in the markets. If U.S. equities face challenges this year due to a recession, we expect fixed income to act as a ballast like it did in the past (prior to 2022), offering income and some potential for appreciation if interest rates decline again. Valuations outside the U.S. and the likelihood of a weakening dollar as other countries raise interest rates could make international equities relatively attractive. Finally, other alternative investments could also provide shelter from market volatility as well. We stand ready to help you navigate the choppy waters ahead and make it through to smoother days on the other side.

[1] https://www.bls.gov/news.release/pdf/empsit.pdf