All-Time Highs

4Q 2024

By Cliff Aque, AIF®, CFA

2024 was a strong year for almost every asset class, with U.S. equities leading the charge. In our last quarterly commentary, we mentioned that the S&P 500 Index had hit 47 new highs in 2024, ultimately adding 12 more before year-end. This rise was driven by optimism around U.S. growth, artificial intelligence, and the potential for deregulation under a new administration. The median forecast at the end of 2023 was for the S&P 500 Index to close at 4950[1], almost 16% below its actual finish, further proving that market predictions are often unreliable.

While many expected bonds to perform well, anticipating rate cuts from the Fed, inflation proved more persistent than expected, leading to fewer rate cuts. The Fed surprised the market with a 50-basis-point cut, followed by two 25-basis-point reductions, bringing the short-term rate down by 1%. However, long-term yields moved higher, particularly in the fourth quarter, with the 10-year Treasury rising 80 basis points, reversing the yield curve inversion that had lasted over two years. This increase was partly driven by concerns over inflation and the uncertainty surrounding Trump’s tariff policies and their potential impact on prices. As a result, the market now anticipates only two rate cuts in 2025.

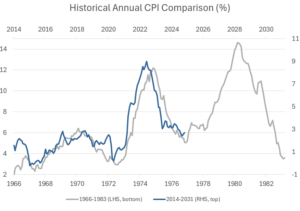

Now, let’s consider the Fed’s dual mandate: price stability and maximum employment. Prices for goods, particularly energy and commodities, have decreased, but services inflation remains elevated. While shelter prices are expected to moderate, they continue to be a significant contributor to overall inflation. The Fed is keenly aware of the inflationary period in the 1970’s and, while the causes differ, the situations have mirrored each other closely. A slight increase in CPI in November will likely have the Fed closely monitoring December’s numbers.

The labor market has been resilient for the past two years but is now showing signs of normalizing, with some potential weakness ahead. Recent gains in payrolls have been concentrated in a few sectors (mainly government), while more cyclical sectors like manufacturing and transportation have seen declines. Given the Trump administration’s focus on government efficiency, a reversal in government hiring is possible. Job openings per person, which peaked at 2 in early 2021, have now dropped below pre-pandemic levels (1.25), and the hiring rate has been steadily declining since 2021, reaching its lowest level since 2013. On the positive side, layoffs remain low, and more people still consider jobs plentiful rather than hard to find.[2]

With the labor market showing stability amid a resilient economy, the Fed is likely to continue its battle against inflation, making “higher for longer” rates a probable scenario. While these higher rates could impact more leveraged companies and lower-wage consumers, the economy overall appears to be coping well. Although U.S. valuations are relatively high, they are concentrated in the largest stocks, with the top ten holdings representing nearly 38% of the S&P 500 by the end of 2024 (compared to 28% at the peak of the dot-com bubble). We expect performance to broaden across different market capitalizations and segments of the markets, underscoring the need for diversification within equities.

After two years of strong returns in the equity market, particularly in large-cap growth stocks, it may be tempting to reduce stock exposure. However, we believe this is a mistake. The average bull market lasts 1,661 days, and we are currently around 810 days into this one. With solid earnings growth projections and an economy that has defied recession forecasts, we encourage you to remain optimistic, diversified, and focused on the long-term.

[1] Source: Goldman Sachs. Investors cannot invest directly in an index.

[2] Source: Bureau of Labor Statistics and St. Louis Federal Reserve