Behavioral Finance: Your Biases And How To Overcome Them

“No amount of sophistication is going to allay the fact that all of your knowledge is about the past and all your decisions are about the future.”

Ian E. Wilson (former Chairman of GE)

“Investing is the act of positioning capital so as to profit from future developments.”

Howard Marks (Economist at Oaktree)

The tension created by these two quotes provides a nice framework for any discussion on behavioral finance and economics. Behavioral Finance is a field of study that combines elements of economics and psychology to understand how and why people behave the way they do in the real world. It assumes that investors are not always rational, have limits to their self-control, and are influenced by their own biases.

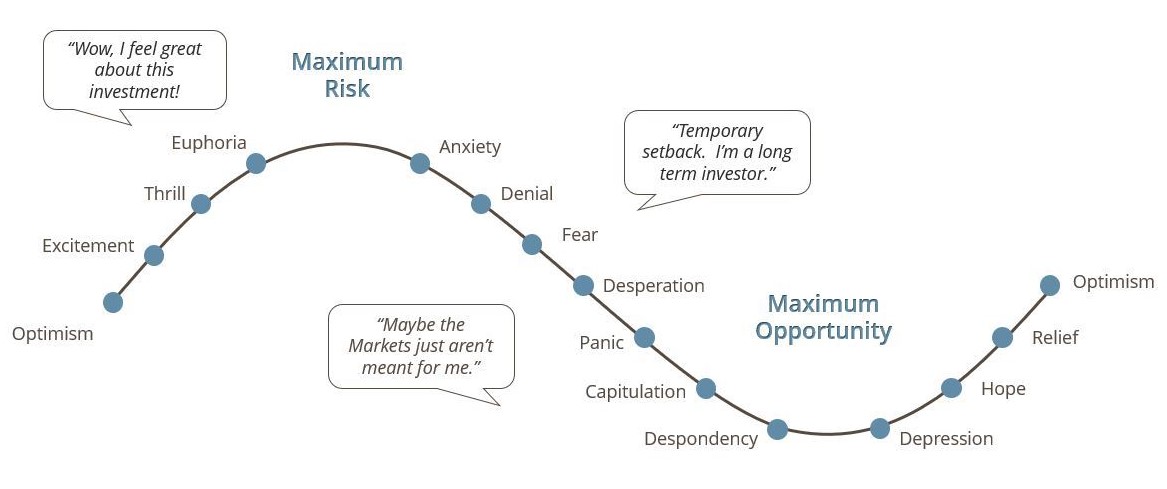

And it’s the uncertainty of events that adds to a normal human issue: investing evokes emotion. Seen in the image below, investing in the markets can often feel like a rollercoaster.

Classic Cycle of Investor Emotions

What factors are currently influencing your emotions about the markets? Are you breathing deep and easy these days? Or when you inhale, have you trained yourself to hesitate for the next shock? Some of our most prevalent concerns closing out 2021 hinge on inflation and taxes. As revenue raising objectives blur lines with wealth redistribution efforts, it appears that the tax burden to pay for government spending will first land on the backs of the most affluent Americans. And it seems a prolonged period of higher inflation may persist until the extra M2 measure of money is fully digested by the economy.

Listed below are a few examples of the cognitive and emotional biases that influence our financial decision-making.

Common definitions in the field of Behavioral Finance/Economics:

Prospect theory refers to a series of empirical observations made by Amos Tversky and Daniel Kahneman (1979) in which they asked people about how they would respond to hypothetical situations involving wins and losses. This allowed them to characterize human behavior in relation to economics.

Loss aversion, first identified by Tversky and Kahneman, is being more afraid of losses than excited by similar gains. Loss aversion is different than risk aversion in that the feeling produced by the outcome is predicated on the expectation held beforehand. The psychological impact of loss can be much more than that of gains.

Nudge theory is the idea that people can be subtly influenced through positive reinforcement and suggestions. Nudging can be applied in behavioral economics, political theory, and behavioral sciences as a method of achieving compliance other than through education, enforcement, or legislation. Example: tax breaks for choices that the government deems positive for society.

Mental accounting is the idea that people think about money differently depending on the circumstances. Example: taking a loan to pay for car repairs instead of using your vacations savings because it’s in a different “bucket”.

While these definitions may leave you feeling convicted, that’s not the point. We are here to remind you of two things. First, you don’t have to navigate any financial challenge alone. Second, not all advice is the same. This brings us back to our examination of behavioral finance, now applied at the firm level. The significant difference between investment philosophies of various advisory firms is in how they handle uncertainty. The knowledge, acceptance, and comfort that we do not have the ability to predict future events is a sort of progressive maturity. With good counsel, you travel the path from acceptance to comfort and are then able to plan accordingly.

If you’ve been a client of our firm for many years, then you have likely heard one of our team members reference our founder, Bryan Brand, with a favorite saying: “Decide in the light what you will do in the dark.” It’s rooted in the conclusion that having a well-planned investment strategy is one of the most critical pieces to successfully reaching investment goals. Conversely, abandoning a well-planned strategy can be costly.

But again, you are not alone. If these thoughts of mine have found their way to your email inbox, then chances are a team of experts thinks of your family more often than you realize. This is meant to be a source of confidence and encouragement. Speaking truthfully, the trajectory of your life is remarkably good. And whatever the next hurdle, working with a group of professionals that have no emotional bias is an often-overlooked benefit. The team here seeks to be a positive wind at your family’s back for generations of kids and grandkids.

So rather than let the unknown darken our minds with anger, fear, or paralysis, consider using thankfulness as a shield. With good, intentional planning, there will be ways to protect your family. The mosaic of experts at Brand are constantly thinking of strategies that reduce risks, insulate your portfolio, and take advantage of opportunities when they exist. All this to positively affect the trajectory of your family’s life.

“Where there is no guidance, a people falls, but in an abundance of counselors there is safety.” Proverbs 11:14