Boring, But Miles from the Bottom

1Q 2014

At a summary glance, the first quarter of 2014 looks a bit boring. The S&P 500 finished the quarter up 1.3% (+1.8% total return, including dividends) with the bond market (represented by the Barclays Aggregate Bond Index) posting a total return of 1.8%. During those 90 days, plenty of surprises awaited investors.

March 9, 2009 Dow = 6,547

March 20, 2014 Dow = 15,419

Global markets experienced a meaningful sell-off in January. The Fed took its second tapering step reducing bond purchases by another $10B per month. It would take a third step in that direction later in the quarter. For the record, we applaud those reductions. A second body blow came in the economic figures out of China showing a slowdown in manufacturing activity. Data in the US hinted at a similar slowdown. While many in the US blamed it on the historically bad winter weather, skeptics believed we were in a full-fledged slowdown and that the Fed wasn’t helping by winding down the stimulus.

Emerging markets, which had arguably benefited most over the past several years’ worth of monetary stimulus, reacted decidedly negative to the double-barreled news of a slowdown in China and the drying up of liquidity needed for continued growth in those economies.

As soon as the Olympics were over, Russian President Vladimir Putin, quite impressed with his medal count, surprised the world by deciding to help himself to a piece of another country. The situation, which is still unfolding, has left many wondering if his ambitions and recent success will result in him trying to annex additional territories of other former Soviet states. Anti-government protests elsewhere, including Venezuela, Thailand and Turkey had international investors on edge as the hope for a better regime flickered with the increasingly violent winds of change.

In the end, despite all the turmoil, global markets managed to move modestly higher over the course of the past 90 days, with emerging markets experiencing a big rebound to finish the quarter down only 0.4% after being down more than 7% by early February. Interest rates, which were almost universally predicted to rise following 2013, were actually lower in the first quarter with the ten-year Treasury note yielding 2.72% as of the end of day on March 31st – down from the 3.04% where it stood on December 31st.

Despite the transitory hiccup caused by weather, the US economy continued to post reasonable employment, inflation, manufacturing and retail sales numbers. That said, we appear to remain in a slowly improving environment, rather than the out-sized growth that many analysts predicted we would see by this point in the post-2008/2009 recovery.

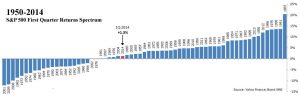

Considering the strength of returns in 2013, we’ll consider the first quarter’s modesty a gift. The graph below puts it in perspective as what our grandparents might have called “middling.”