Bracing for Bad Data

Tomorrow (Wednesday, April 29th at 7:30 am Central) we will see the first estimate of Q1 2020 US GDP. This figure is of particular interest because it represents the first look at how the US economy as a whole fared during the first quarter, which included quarantines beginning in February.

Most forecasters believe the US economy contracted in the first quarter and will continue to contract in the second quarter. While two consecutive quarters of negative real GDP growth is the popular definition of a recession, the National Bureau of Economic Research (NBER; the organization which officially determines whether or not a recession has occurred) defines a recession as a “significant decline in economic activity spreading across the economy, lasting more than a few months.” Either way, absent a significant rebound in May and June, it appears the US economy is likely headed towards its first recession since the 2008/2009 Great Financial Crisis.

That brings us to the first purpose of this note: prepare yourself now for the superlative headlines that may flash across TV screens tomorrow.

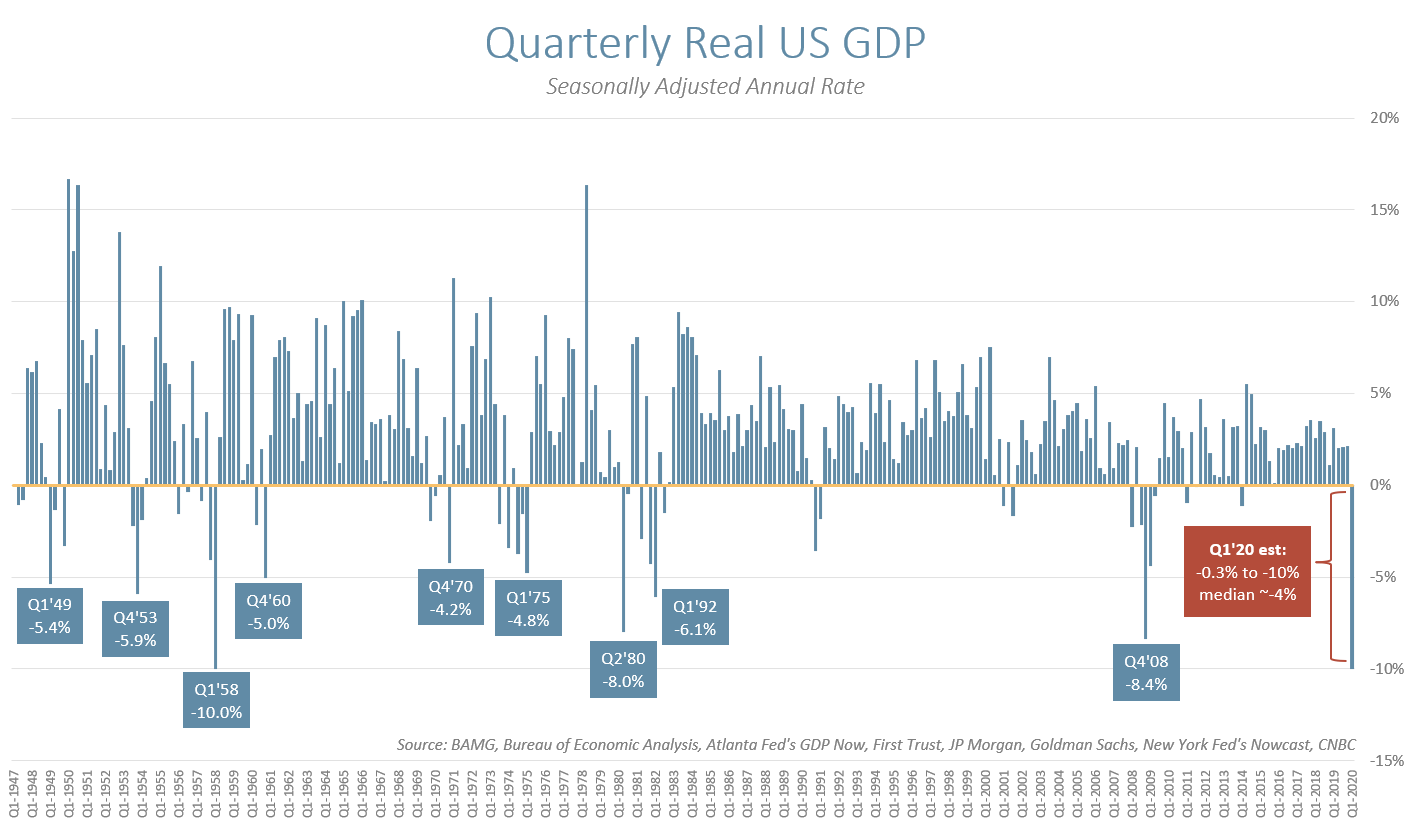

Here is some perspective on the data. The range of estimates for Q1 real GDP is large (we have seen anywhere from -0.3% to -10.0%), but the consensus is somewhere in the -4.0% vicinity. Historically speaking, that is a very large range – but that is what tends to happen in a period of great uncertainty, like what we have experienced in these early stages of the coronavirus pandemic.

Below is a chart that shows real US GDP since the Bureau of Economic Analysis (BEA) began keeping track of quarterly figures in 1947. If the level comes in better than -8.4%, we expect to see headlines like “Worst quarterly GDP since 2008.” If the print is worse, headlines could read “Worst quarterly GDP on record.”

It is important to understand that this data is backward-looking and that markets have already anticipated a large decline – that’s why markets sold off so much from February 19th through March 23rd.

This brings us to our next point: brace yourself for pundits to move on to discussing how bad second-quarter GDP might be (which will be reported in about 90 days).

Q2 GDP will also likely show a negative number (and possibly worse than the Q1 figure tomorrow, since a larger portion of Q2 will be impacted by the shutdown). Early estimates are for Q2 GDP numbers ranging from -9% to -50%, but these early estimates are difficult to interpret, as the calculation of Q2 GDP is dependent on the final Q1 figure. Additionally, the second quarter is only one-third of the way complete. For both of these reasons, discussing Q2 GDP estimates seems challenging at this point.

All in all, we hope that tomorrow investors will resist the knee-jerk reaction to trade once the data and the inevitable comparisons begin to hit the headlines. Sticking with a well-designed plan, maintaining your allocation, rebalancing and tax-loss harvesting where appropriate all continue to be great playbook strategies and tactics for long-term investors in volatile times.