Climbing the Wall of Worry

2Q 2014

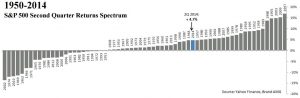

Equity markets started off slowly in the second quarter (S&P 500 was flat for the quarter until May 20th), but ended up accelerating their overall advance from the first quarter, finishing the quarter +4.7% (+5.2% including dividends). Large and mid-sized companies continued to outperform smaller ones, while value outperformed growth. Following a brutal winter, which contributed to a -2.9% first quarter GDP figure and shook the confidence of many investors, it appears the US is back on a positive economic trajectory. Recent housing data, vehicle sales, manufacturing figures, employment and rail carloads are all exhibiting stability and/or trending higher.

Internationally, the presence of geopolitical tensions, which started to bubble up in the first quarter following the Olympics, escalated in the second quarter as Russia showed it wasn’t satisfied with just annexing the Crimean Peninsula. Late in the quarter, the Sunni extremist group ISIS/ISIL (so extreme that even al-Qaeda is scared to associate with them) began to take control of towns in Syria and Iraq, causing even the unlikeliest of allies (US and Iran) to consider working together. Surprisingly, with all the international turmoil, oil (Brent crude) rose only $10 (from $105 at the start of the quarter to $115 at the peak), while gold rose only 3%. On the positive side, we would note that the currency crisis that had been brewing in emerging market countries in the first quarter began to abate in the second quarter, with the emerging market index +6.7%. Additionally, during the quarter the European Central Bank decided to try to shift the European recovery into a higher gear by moving the deposit rate below zero (penalizing banks for not lending).

Lastly, we would note that fixed income markets maintained steady growth during the second quarter, with the Barclays Aggregate Bond Index +2.0% as the ten-year Treasury yield trended lower, averaging 2.62% in the quarter vs. 2.77% in the first quarter. With inflation starting to tick modestly higher and the unemployment rate nearing the Fed’s earlier target, many are anticipating the beginning of the end of near-zero-percent interest rates in the US. If the Fed continues down the path of tapering bond purchases by $10 billion at every FOMC meeting (currently at a pace of $35 billion in monthly purchases, from $85 billion monthly as recently as December 2013), its bond buying program will expire in either October or December, with many expecting the Fed to hike interest rates by early to mid-2015. This transition is front and center in the market’s mind.

We believe all the economic and geopolitical surprises, as well as the divergence seen in different market caps and styles underscores the importance of the task of staying diversified and disciplined. With that, we would remind investors that we are due for volatility. So far the worst we’ve seen this year was a 5.8% pullback (Jan. 15th – Feb 2nd) in the S&P 500 (versus the average intra-year pullback of 15% since 1980). That volatility may come into play as we approach the Fed’s transition and midterm elections. That said, despite being near all-time highs in the stock market, we are not overly concerned about equity valuations, and would note that we can witness long periods of persistent strength. Case in point: on June 20th, we saw the 67th all-time high in the last 15 months (approximately one for every 4.7 business days).