Coronavirus & Market Update

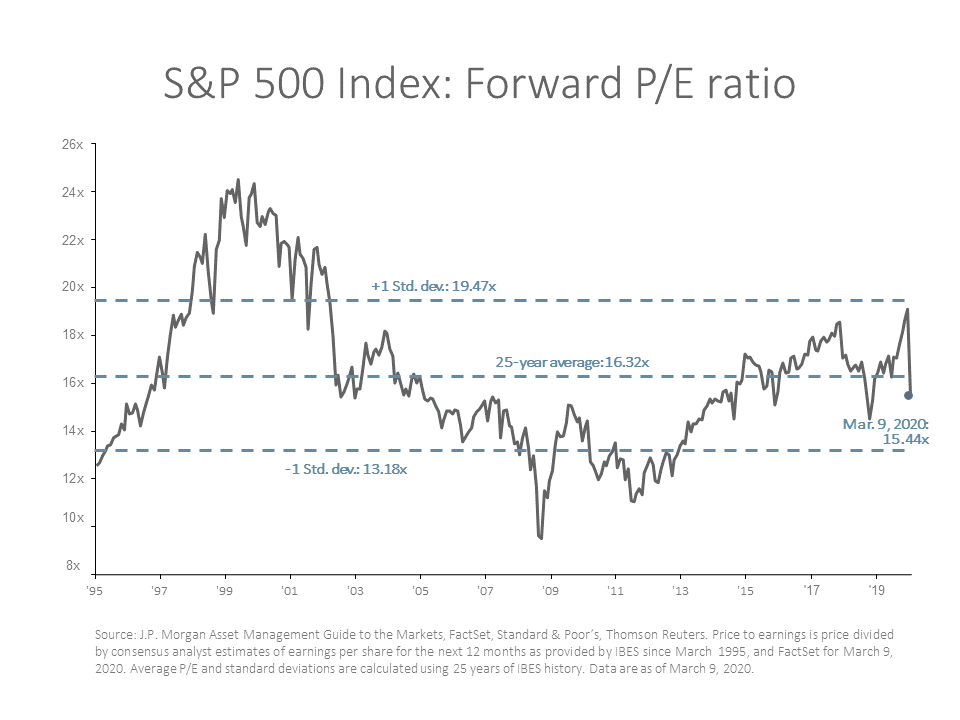

| Yesterday, global stock markets were again selling off as fear of a coronavirus-induced recession continued to spread. What had been a steady drop in the price of oil due to a general slowdown of global economic activity, evolved into a much larger drop over the weekend when Saudi Arabia decided to start a price war with Russia. Now, with the price of oil dropping nearly 25% in a day, this additional confrontation has markets even more worried about the future. Let’s address some of the market’s concerns. First of all, when we were setting new highs (only 12 trading days ago), the market was getting somewhat expensive by historical standards (see figure below). |

| For context, the 25-year average forward price-to-earnings multiple for the S&P 500 Index (representing the largest 500 companies in the US) is around 16.3x earnings. As of the market’s most recent peak (February 19th), the multiple had drifted to nearly 19x. As of Monday’s close, the S&P 500 is down 18.9% from the peak, and the current multiple is roughly 15.4x. Granted, many earnings estimates will be cut over the next few weeks and possibly months as analysts and management teams quantify the impacts of the slowdown on their business, but the main point is that the market is no longer what many people considered “expensive”. |

Additionally, we believe the economic damage done by the spread of the coronavirus will be temporary – not permanent. A fully coordinated response might look like a combination of monetary stimulus (e.g. the Fed lowered interest rates last week to ease what had been a tightening in credit conditions, and we could see further rate cuts or other methods to ease credit markets) and fiscal stimulus (in the form of targeted tax relief and possibly other policies to help businesses to stay afloat during a transitory exogenous shock). Add to that a backdrop in which businesses increase efforts to sanitize doorknobs and handrails, and healthcare professionals are adequately supplied with all necessary testing kits (which may be only weeks away), and we have a significantly better outlook for the economy. The restocking effect alone from such a rebound could be massive. |

We say all of this not because we have insight into what the future holds, but because we have confidence that we are coming from a position of relative strength, and things will ultimately get better. Remember that in 2008, the concern wasn’t a temporary event – the concern was the total systemic collapse of capitalism. We know that at least up until the past couple of weeks, the US economy was in pretty good shape, meaning if we do go into a downturn or recession, we are already in a better position than we were in 2007-2008. Last week’s monthly jobs data indicated nonfarm payrolls were +273,000 (a big number) in both January and February, according to the Bureau of Labor Statistics. Manufacturing and service index levels were still pointing toward economic growth. Housing starts have been strong lately, and retail sales in January were +4.4% year-over-year (US Census Bureau). Maybe most importantly, bank balance sheets are stronger than ever as a result of all the post-2008-crisis regulations that required them to stash away higher amount of tier-1 capital (the most solid financial instruments available, like cash and US Treasury bonds). Likewise, consumer balance sheets contain much less debt than they did before the global financial crisis. So, we are certainly not in a position of systemic weakness. |

While it appears stormy now, we admit that we don’t know what the path will look like, but we firmly believe we will see the sun again. Market history is littered with scary episodes for investors. Some of the more notable recent ones are… – The US Debt Downgrade in August 2011, which resulted in a 7% market drop in one day. – “Flash Crash” on May 6, 2010, which saw the Dow drop 9% in a matter of minutes. – “Black Monday” in October 1987, which saw the market down over 20% in a day. We know people will get sick with the coronavirus, and there’s nothing we can do about that as investors. What we can control is how we react as investors and to resist the urge to abandon our principles of diversification. Instead, we can take advantage of the opportunities that the market gives us – to rebalance where appropriate, capture losses where available for future tax assets, and use historically low interest rates to refinance any higher cost debts. |