Economic Ripples

3Q 2021

It’s impressive to see how far we’ve come since the pandemic began, but many storylines continue to unfold. From near complete global lockdowns to the discovery, large scale production, and now global distribution of the vaccine, slowly but surely, progress is making its way through the global economy. Early on, the rebound in the US economy was slow, but the reaction in the stock market was quick, due in large part to the vast fiscal and monetary support provided, and the anticipation that eventually better days were on the horizon. Since the market bottom in March of 2020, the only pullback of any significance was in September 2020 when the market fell 9.6% from the previous high. Since then, the market has moved steadily higher and we hadn’t seen much departure from that trajectory…until this September.

As we continue to recover, support for additional stimulus is fading and politics have become more combative, especially around a trifecta of infrastructure spending, government funding, and the debt ceiling. Coupled with recent hints by the Federal Reserve of tapering (reducing) bond purchases in the market, the backdrop is evolving from an economy supported by massive stimulus to one that must eventually stand on its own two feet. While this is good news in the long term, unfortunately markets react to transitions like these with volatility – a virtual tug-of-war between buyers and sellers as traders attempt to take advantage of short-term market movements from negative headlines.

Inflation continues to be one of the bigger questions on the minds of investors – particularly whether it will be temporary or longer lasting. Much of the reason for rising prices is due to supply and demand imbalances. When the world was shut down, people needed less, and companies scaled back on production. But as the world began to open up, companies were unable to bring production back up to levels sufficient to meet the rapidly rising demand levels. The result was rising prices and this condition will only be solved by a normalization of labor markets (getting people back to work, both in the US and abroad). When that bottleneck is fixed, more goods will be produced and processed (i.e. shipped) more efficiently. The ripple effect will allow prices to fall back toward their normal “equilibrium” levels, though they may not get all the way back to where they were.

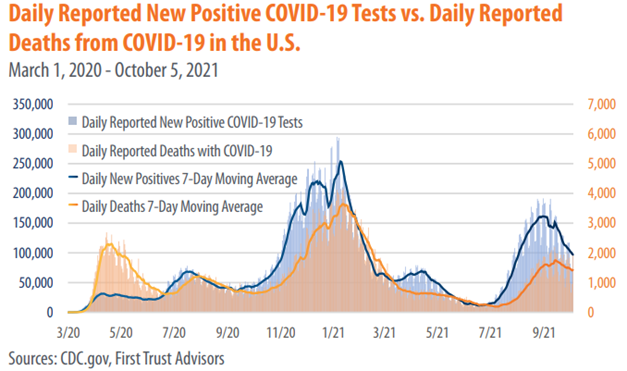

JP Morgan estimates that nearly 85% of Americans have some immunity to COVID-19 between infection and inoculation. Merck’s recent news unveiling a pill for COVID patients that reduces the probability of hospitalization and death could be another game changer. Additionally, every day the world is better adapting to operate in a COVID world. As vaccines and treatments reach the rest of the world, this should help normalize foreign labor markets, which will help reduce supply shortages in many components that are contributing to inflation.

The bottom line is that the global economy continues to heal, but the path may be bumpy as we transition from a very supportive backdrop to one with less stimulus. If labor markets remain dysfunctional, inflation could persist for a while longer. Under that scenario, since inflation negatively impacts cash and fixed income the most, it’s particularly important to ensure that investors have the appropriate asset allocation. With valuations of US stocks above average and interest rates low, the need for a disciplined investment strategy, complete with tactics like rebalancing and tax loss harvesting, is of paramount importance.