From Lemons to Lemonade

4Q 2018

In some years it’s easy to be an investor. In other years, markets will test your resolve. 2018 was a “testy” year globally. Following solid gains in 2017, markets began to hit turbulence in February. For a little while afterward, US markets moved higher, while international markets flattened out. But then early in the fourth quarter we saw a large decline in both US and international stocks, which was exacerbated by an even larger drop in December.

Christmas Eve marked the low point for most stock segments, with most groups hitting corrections (defined as a drop of 10% or more from their most recent high) or even bear market territory (defined as a drop of at least 20% from the high). Media hysteria ensued, with TVs flashing and emails flying from perma-bears who have been calling for the next stock market crash for more than ten years now.

Several reasons for the pullback have been cited, but generally they fall into three themes: lower expectations for economic growth and corporate profits, less appetite for fiscal or monetary stimulus, and political uncertainty. However, none of these three themes last forever, and it’s important to keep the recent market movements in perspective. This decline is only the most recent in a long line of pullbacks throughout history. Yes, this one felt a little more substantial than others because it happened so quickly and hadn’t happened in such a long time, but in reality, stock market volatility of this magnitude is far from unprecedented.

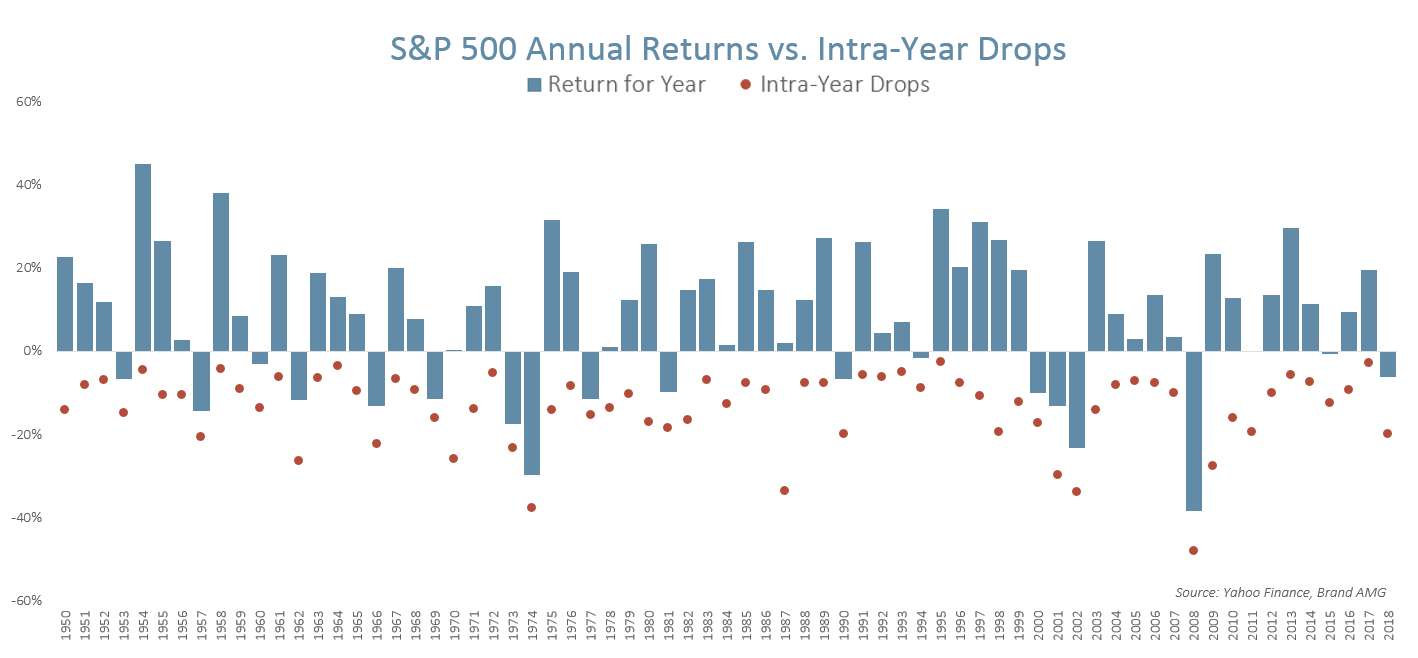

The chart below shows that intra-year declines in the S&P 500 have averaged nearly 14% since 1949. And those drops have breached the 15% threshold 22 times in the past 69 years – or nearly once every 3 years! The fact that we haven’t had a drop of even 15% since 2011 is what is most remarkable!

It’s also important to note that although the broad US stock market (Wilshire 5000) finished the fourth quarter -14%, most diversified investors fared better. And this is on the back of several years of positive gains, including the outsized gains of 2017. A basic 60/40 investor who rebalanced annually would have been up roughly 188% through September 30th since the end of the financial crisis. While it’s never fun to experience volatility of this sort, it helps to keep the damage in perspective.

The last thing we would point out is that on average, performance following a pullback of this magnitude is quite positive. Using data from the S&P 500 index since 1949, we find that the median return on the index exactly two years after the index first hits the -15% threshold is +18.0% (or 8.6% per year), and the median return two years after it hits the -20% threshold is +32.6% (or 15.1% per year)…and this is before dividends, which often add another 2%+ per year. Turns out that Warren Buffett’s advice to buy stocks when they are “on sale” largely pays off!

Merriam-Webster defines discipline as “a rule or system of rules governing conduct or activity.” The purpose of establishing investment discipline (like creating an Investment Policy Statement) is to decide in the light what we will do in the dark. We encourage investors to stay disciplined during difficult times and use those opportunities to turn lemons into lemonade. Actionable items include rebalancing across the portfolio (where applicable) and harvesting investment losses in taxable accounts (which creates an asset that can be used to offset some of your tax liability).

We took advantage of some great opportunities in the fourth quarter, and while we hope for a return to the “easier” years in 2019, we stand ready to make more lemonade if opportunities present themselves.