Grand Reopening

2Q 2021

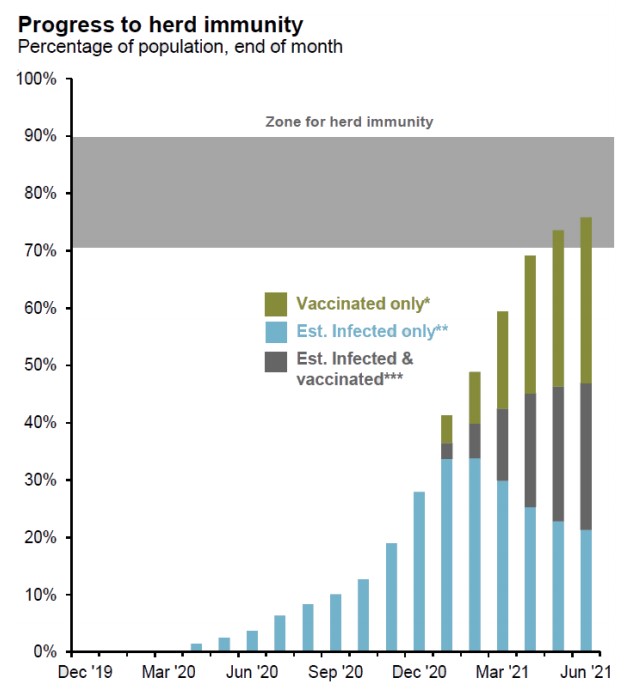

The second quarter saw the continuation of a powerful economic recovery due to fading of the pandemic and massive fiscal and monetary stimulus. US vaccinations have increased significantly with 46% of US adults now fully vaccinated, 54% with at least one dose, and 86% of the population over age 65 having received at least one dose. According to JP Morgan Asset Management (see image below), this moves us inside the range of 70-90% of the population many experts estimated we needed to achieve “herd immunity”.[1] This is good news for the economy, as consumers are ready to get out and spend money. Payrolls, industrial production, and manufacturing are expanding, and businesses are eager to hire workers. Analysts estimate GDP grew 8-9% in the 2nd quarter.

As anticipated in our last quarterly market summary, rising inflation figures continue to be a topic of debate. A portion of the inflation figure is undoubtedly due to easy comparisons. For example, when you compare $70 oil now to $20 oil a year ago, that’s a 250% increase, which drives the inflation figure higher. Additionally, disrupted supply chains and labor market distortions have contributed to inflationary pressures, but the inclination for those forces to abate over the next several months is high. All that said, most economists are only looking for inflation levels to be 3-4% over the coming year or so, then fall back toward the Federal Reserve’s 2% longterm target over time – nowhere near the levels we saw in the 1970s and 1980s.

US large cap stocks (represented by the S&P 500) finished the quarter +8.5% including dividends, with growth stocks +11.9% and value stocks +5.2%. Small sized companies were +4.3%. Earnings growth remains strong for US stocks, with a record 87.5% of companies beating analyst estimates in the first quarter, and analysts raising their second quarter earnings estimates at the highest rate on record. International stocks were also positive for the quarter, though the performance lagged behind that of the US, largely attributable to the delayed reopening of those economies. International developed market stocks were +5.2%, while emerging market stocks were +5.0%.

Interest rates rose much of the fourth quarter of 2020 and first quarter of 2021 (the 10-year Treasury yield climbed from 0.69% on September 30th 2020 to 1.74% on March 31st, 2021), but fell in the second quarter (to 1.45% on June 30th) reflecting reduced inflation expectations compared to earlier in the year. The drop in interest rates enhanced the performance of bonds, with the Bloomberg Barclays US Aggregate Bond Index returning 1.8% for the quarter. It’s always difficult to predict how the rest of the year will unfold, but we appear to have the tailwind of a positive economic backdrop at our back. Several unknowns still exist including further stimulus, tax policy, and inflation. If inflation does persist, we remain well-positioned to capture any upside from it given our value tilt and international stock exposures. For all of the unknowns, we encourage investors to stay diversified and disciplined, knowing that when (not if) the markets become volatile we will do what we always do to take advantage of those opportunities.

[1] Source: Centers for Disease Control and Prevention, Johns Hopkins CSSE, Our World in Data, J.P. Morgan Asset Management.

*Share of the total population that has received at least one vaccine dose.

**Est. Infected represents the number of people who may have been infected by COVID-19 by using the CDC’s estimate that 1 in 4.6 COVID-19 infections were reported.

***Est. Infected & vaccinated assumes those infected equally likely to be vaccinated as those not infected. On 5/6/21, JPM moved up the threshold for herd immunity from 60-80% to 70-90% based on the comments by Dr. Anthony Fauci that the prevalence of more contagious variants have pushed up the target herd immunity threshold for the U.S.

Investors cannot invest directly in an index.