Implications of Low Interest Rates for Investors

One of the far-reaching impacts of the nationwide shutdown due to the coronavirus has been on interest rates. The sudden slowdown in economic growth, the Fed’s emergency monetary policy, low inflation, and longer-term growth trends have collectively pushed Treasury yields to historic lows, which tends to frustrate investors. And while the economy is beginning to reopen, it may take much longer for rates to fully recover – if they do at all. For this reason, it is important for investors to have perspective on interest rates and what they could mean for investment portfolios going forward.

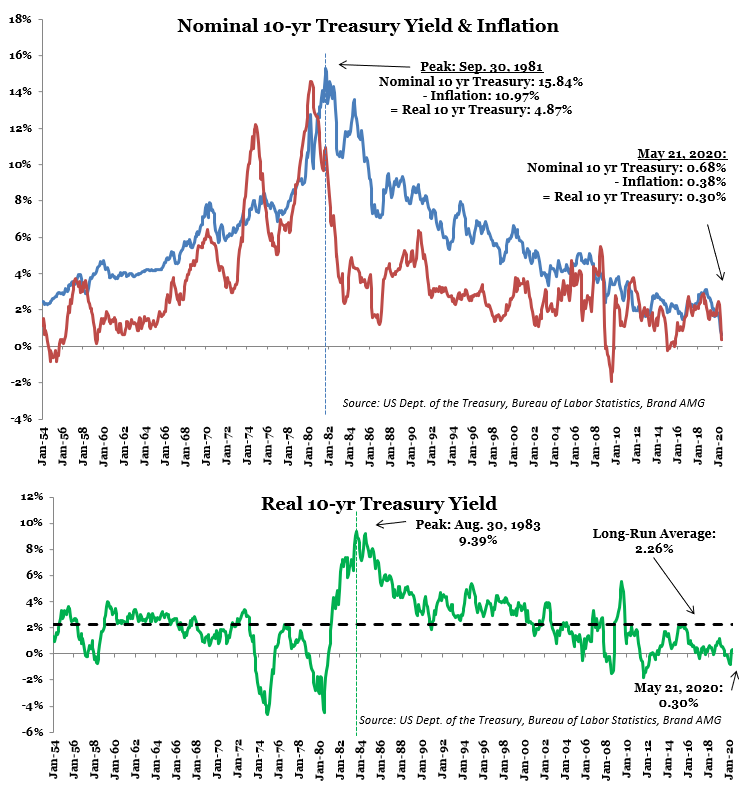

Low rates are nothing new. Although they were high in the 1970s and 1980s, they were lower before then, and have been declining steadily for almost 40 years since the 10-year Treasury yield peaked at nearly 16% in 1981. Below are two charts showing 10-year Treasury bond yields in both nominal and real terms, as well as inflation. Nominal interest rates are the rates you see quoted every day on TV or your favorite financial news website. Real interest rates are simply the nominal rate minus inflation – so the real rate can be thought of as the “after-inflation” or “inflation-adjusted rate”. You’ll notice from the charts that all three – the nominal interest rate, inflation, and the real interest rate – have trended lower over the past nearly four decades.

Why have rates been on a downtrend for so long?

First, it must be understood that the reason interest rates ever got as high as they did in the early 1980s was because of the high levels of inflation of the 1970s, which required Federal Reserve Chairman Paul Volcker to raise interest rates to such high levels in an effort to break the trend of rising inflation. The tactic worked, but resulted in all of us now, 40 years hence, using an analytical starting point that was much higher than where rates would have been if we hadn’t experienced an Arab oil embargo and other factors that resulted in the high rates of inflation from the 1970s.

Beyond just Fed policy and the normalization of inflation, many other causes have been attributed to this long-term downtrend. Generally speaking, the real 10-year Treasury rate is viewed by most economists to approximate short-to-intermediate-term economic growth rates (see the chart below depicting real interest rates and actual US GDP over the subsequent two years). Thus, as the US economy matures, it is natural for economic growth rates to slow down, which in turn should cause the real 10-year Treasury rate to naturally drift lower.

Globalization of financial markets and developed country demographics have likely also played a role in the decline of interest rates, because when demand rises for a bond, the price goes up, but the interest rate you earn on the bond goes down. This occurs because while you paid more for the bond up front (price went up), the interest payments you will receive are fixed (so the overall rate of return you earn on the initial investment goes down). As financial markets have matured over the past several decades, it has become easier for foreign investors to access other countries’ markets. The aging population of the world’s developed economies has contributed to all of those countries’ Treasury bond yields moving lower, as allocations for older populations naturally shift to less aggressive portfolios (meaning more bonds in their portfolios).

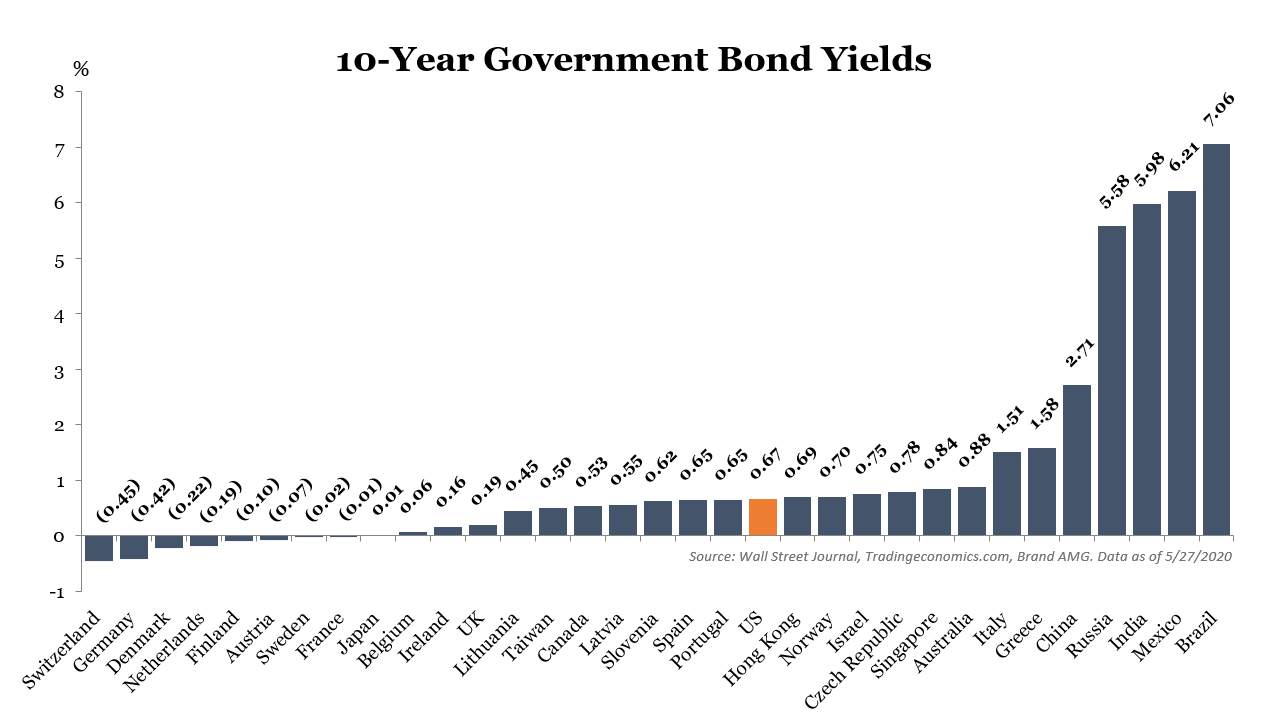

Furthermore, as the US dollar has continued to solidify itself as the reserve currency of the world, many foreign investors, including large foreign insurers, sovereign wealth funds, and central banks invest in US Treasury bonds as a form of holding “risk-free” assets and as currency reserves to help control their foreign exchange rates. Compounding the demand for US Treasury bonds is the fact that foreign central banks are buying large amounts of their own countries’ bonds to keep their domestic interest rates low. With other developed economies like Europe or Japan keeping their current bond yields even lower than the US (see chart below), our relatively higher interest rates attract other foreign investors.

It’s hard to overstate the importance of interest rates across the economy. However, it’s important to distinguish between the many different crosscurrents for investment portfolios. On one hand, low rates hurt savers, especially those who rely on interest income. On the other hand, low rates are great for borrowers including homeowners and businesses. These cheaper rates should help boost growth once the economy reopens and the financial system stabilizes.

At the macro level of the economy and markets, interest rates have other important implications:

- Interest rates are a signal about economic health.

Over time, faster economic growth should normally spur inflation and push up both real and nominal interest rates. Conversely, low interest rates suggest worrisome expectations of future growth. From this perspective, it’s no surprise that rates suddenly declined due to pessimism and uncertainty about COVID-19 and the future in general.

- How interest rates move relative to one another is important too.

The yield curve inverted last year (i.e. long-term rates were lower than short-term ones), suggesting that there were stresses building in the economic and financial system. While it’s doubtful that the yield curve predicted a coronavirus-induced recession, it does suggest that markets didn’t believe the Fed could maintain their higher short-term rates. With the Fed having lowered short-term rates back to zero, the yield curve has returned to a more “normal” upward-sloping shape, which is a positive signal.

- Low interest rates tend to boost stock market valuations.

While this is not a one-to-one effect, and often depends on why interest rates are low, investors are constantly facing a decision on how much to allocate between stocks and bonds. Because, generally speaking, stocks are riskier and more volatile than bonds, investors require a higher expected return in order to invest in stocks. When the difference between what you know you can earn in a bond (the yield) and what you think you can earn in a stock (consisting of both dividend yields and growth in the company’s business) is relatively low, investors tend to allocate more to bonds. An example of this type of situation would be an environment where interest rates are high and stock valuations are expensive. However, when interest rates are very low, as they are now, it creates a lower relative hurdle for investors to embrace stocks.

The bottom line is that interest rates are near historic lows, which many investors find disconcerting. And while this may contribute to lower expected returns for a diversified portfolio than in the past, the positive is that this should help boost the economy as it reopens, as well as the profitability of corporate America by making it less expensive for companies to borrow money for expansion.

Meanwhile, despite the frustration of low current yields, long-term investors should remember that bonds serve the important role of portfolio stabilizer, especially during periods of uncertainty in the markets. This is because the other ramification of falling interest rates is a rise in bond values. Perhaps there is no better evidence of the importance of their role in a portfolio than this year, as diversified bonds outperformed all other asset classes during the February-March meltdown.