Musical Fears

February 18, 2016 – It’s been a rough first six weeks of the year for investors. After many months of fears over falling oil prices, once the calendar turned to the New Year, volatility in Chinese stock markets added to global concerns. Now, with oil prices and Chinese markets relatively stable, why are markets still nervous? The answer recently shifted to a new fear – accommodating central banks.

February 18, 2016 – It’s been a rough first six weeks of the year for investors. After many months of fears over falling oil prices, once the calendar turned to the New Year, volatility in Chinese stock markets added to global concerns. Now, with oil prices and Chinese markets relatively stable, why are markets still nervous? The answer recently shifted to a new fear – accommodating central banks.

Since the end of the 2008-2009 financial crisis, most central banks around the world have been employing policies to try to stimulate economic growth, such as keeping interest rates low. For many years, this was viewed as a positive by the markets. However, the introduction of negative interest rates (first used by the Europeans, and recently imposed by the Japanese) are having an adverse effect on the profitability of the banking sector. And because the banking sector plays a unique role in market psychology, weakness in bank stocks is having an out-sized effect on the rest of the markets.

However, in times of stress it’s important to note the distinction between the two primary flavors of market fears: profitability fears and solvency fears. The first type (profitability) is the root of the more frequent episodes of market volatility and corrections. It happens when markets become concerned that a company (or industry) is entering a period of turbulence caused by either a slowdown in customer demand or an increase in costs (sometimes in the form of regulation changes). Both of these factors lead to lower overall profitability – a short-term phenomenon.

The second type (solvency) is less frequent and stems from fear that a company (or industry) may be forced into bankruptcy or restructuring. These are periods like the 2008-2009 financial crisis and the 2011-2012 Eurozone debt crisis, during which several European countries faced the collapse of financial institutions. The important thing to keep in perspective is that negative sentiment for bank stocks focused on the income statement (i.e. profitability) is much less significant than fears of bank balance sheets (i.e. solvency).

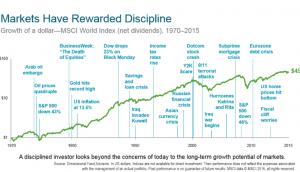

I was reminded recently of a 1985 paper titled “Does the Stock Market Overreact?” where the authors (who would later become professors at the University of Chicago and DePaul University) explored the differences between classical economic theory (the idea that people make rational decisions all the time) and behavioral finance (the idea that people don’t always react rationally). The conclusion was that people tend to overreact to “unexpected and dramatic news and events”, which causes markets to fluctuate between optimism and pessimism and results in stock prices being either higher or lower than they deserve to be.

In times like these, it’s important to avoid worrying about the things we cannot control, and instead stay focused on the things we can control: our own behavior, which if managed correctly, in the end will yield better investment results by taking advantage of opportunities to re-balance and tax loss harvest, where available. These seemingly small actions can end up paying big dividends for investors down the road.