Not Out of the Woods Yet

4Q 2023

If you just looked at market returns at the end of the year, you would never know the bumpy ride we took to get there with stocks up 26.3% and bonds up 5.5%[1]. The year saw not only four more rate hikes, bringing the federal funds target rate up from 4.5% to 5.5% (the highest in 20 years), but also turmoil around the US debt ceiling, bank failures, a downgrade to the US credit rating, and a war in Gaza. If one knew all those things were going to happen, it is doubtful they would have predicted the market returns we had in 2023.

After the third quarter, we mentioned that the markets were understandably down a little bit as investors digested the Federal Reserve’s (“Fed’s”) “higher for longer” comments, meaning that we were going to have higher interest rates for longer than people expected. But then in the fourth quarter, the Fed released its minutes revealing that they may be finished hiking rates and see three rate cuts in 2024 for a total of 75 basis points. This news sent both stock and bond markets on a furious rally, with the S&P 500 Index in positive territory for nine weeks in a row to end the year – its longest winning streak since 2013. The bond market staged a similar rally after the 10-Year US Treasury hit 4.99% in mid-October only to plunge 111 basis points to 3.88%, almost exactly where it started the year!

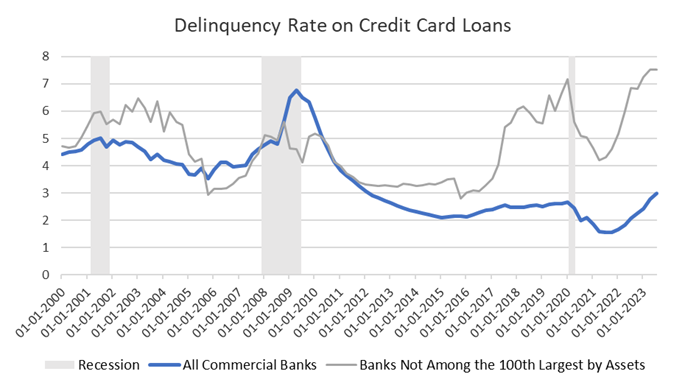

Despite the Fed raising interest rates by 525 basis points in this cycle, the consumer and job market have remained resilient driving the narrative that the Fed might be able to engineer a soft landing for the economy. However, both consumption and job creation can change very quickly as people may decide to stop spending or hiring. Consumption, which makes up almost two-thirds of nominal GDP can slow quickly leading into a recession and there are signs of stress for consumers as credit card and auto loan delinquencies have been steadily increasing since the end of 2021. While the absolute levels are not distressing, the trend is. The Saint Louis Fed found that the percentage of adults in financial distress from credit card debt hit 4% in the third quarter, a level last hit during the financial crisis[2].

Source: St. Louis Federal Reserve, Brand AMG. Data is quarterly, seasonally adjusted.

The unemployment level remained below 4% since the Fed started hiking, giving them plenty of buffer to fight inflation and raise rates. However, we are starting to see softness materialize as the number of job openings has continually declined since March 2022, and the monthly numbers have been revised lower in ten out of the last eleven months. Corroborating this softness since May 2022 is a steady increase in layoffs and a decline in the number of people quitting, meaning that it is getting harder to find a job. Finally, jobless claims tend to be a lagging indicator for a recession and generally start to move up after we are already in a recession.

Interestingly, up until that October rally, most of the S&P 500’s return had been driven primarily by seven stocks, coined “The Magnificent Seven.” These stocks are Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, Nvidia, and Tesla, and the group now comprise 25% of the S&P 500. However, since October we saw market breadth increase, meaning more stocks participated in the move upward, and the Magnificent Seven have been outpaced by small and mid-cap stocks since then. This is yet another highlight of the importance of diversification within our portfolios.

The markets gave us a wild ride in 2023, but a pretty good outcome for most asset classes, with most erasing the losses of 2022. The lesson we take from it is that it is important to be invested when the markets move up, because you never know when that will occur. As mentioned above, staying diversified is similarly important as different parts of the markets move at different times. Our job is to help you stay on the ride and ignore the noise, which there is bound to be plenty of in 2024.

[1] As represented by the S&P 500 Index and the Barclays U.S. Aggregate Index. Investors cannot directly invest in an index. Source: Morningstar Direct.

[2] Source: St. Louis Fed.