Policy Rollercoaster 4.0

1Q 2025

By Cliff Aque, AIF®, CFA®

If you’ve been following the news this year, you may have found yourself thinking, “Let me off this ride.” A surge of executive orders—spanning the federal government, immigration, citizenship, foreign policy, law enforcement, and trade—has made the start of 2025 unusually turbulent.

Following President Trump’s re-election in November 2024, markets initially rallied on expectations of deregulation and tax cuts. But those require Congressional action—and time. In the meantime, the administration has focused on areas it can affect unilaterally: reducing government inefficiency, ramping up deportations, and, most consequential for financial markets, imposing significant new tariffs.

While the headlines have been dramatic, context matters. Through April 10, the S&P 500 experienced six daily moves of ±2%—compared to just eight total across 2023 and 2024 combined[1]. Those two years were abnormally calm and delivered strong returns, especially relative to 2022, which saw 46 such swings. This year’s pullback—18% peak to trough—feels sharp but isn’t unusual: over the past 45 years, the S&P has averaged a 14% annual drawdown.

Most of the pain has been concentrated in the largest names. The so-called “Magnificent 7”[2] are down more than 18% through April 10, while the other 493 companies in the index are down just 4.3%. As we noted last quarter, the top 10 companies made up 38% of the S&P 500 at the end of 2024—the highest concentration since the dot-com era. Even after the recent selloff, they still represent nearly 36% of the index, underscoring the importance of diversification[3].

While the S&P 500 is down a little over 10% year-to-date, international equities and large-cap value have fared better, and fixed income has provided a buffer with positive returns. Notably, European equities reached new all-time highs in Q1—their first since 2000—even as U.S. stocks stumbled.

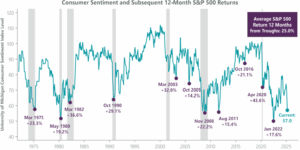

Tariff uncertainty has weighed heavily on sentiment among both businesses and consumers. Consumer confidence plunged in March and April, with the University of Michigan’s Index of Consumer Sentiment falling to 50.8—the second-lowest reading since records began in 1952[4]. The only lower point was in June 2020, during the pandemic, when it hit 50. Investor bearishness—expecting market declines—has also climbed into the top decile of historical readings. But history offers perspective: over the past 50 years, when consumer confidence has dropped sharply, the S&P 500 has delivered an average 12-month return of 25%.

Business sentiment has also softened, but the labor market remains resilient. Jobless claims are still low. While the newly created Department of Government Efficiency (DOGE) has made headlines, related layoffs amount to roughly 280,000—just 6% of the federal workforce. Even so, unemployment ticked up just 0.1% to 4.2%[5]—well below the 50-year average of 6.1%. March payrolls showed continued strength with 228,000 jobs added.

While President Trump appeared content to let markets fluctuate, moves in Treasury yields and the dollar may have prompted a shift. The administration announced a 90-day pause on tariffs with most countries after the 10-year Treasury yield surged from 3.87% to 4.53% in early April[6]—potentially signaling that U.S. debt is no longer seen as a safe haven. At the same time, the U.S. dollar fell to a three-year low (as measured by the DXY Index), further reflecting investor uncertainty. Both markets appeared to stabilize on April 11, when Boston Fed President Susan Collins told The Financial Times that the central bank stood ready to support financial stability (sometimes called “the Fed put”).

While the tariff pause and Fed put may quell some investors’ anxieties, we expect volatility to persist until there’s more clarity on tariffs. But this isn’t the first time markets have reacted sharply to policy shifts—and it won’t be the last. Historically, sharp selloffs driven by uncertainty have often created compelling entry points.

As always, we encourage you to stay focused on your long-term objectives and tune out the short-term noise. If you’d like to revisit your portfolio or strategy—or simply want a conversation—we’re here.

P.S. The original version of this note was simply Policy Rollercoaster—but after the past week’s events, version 4.0 felt more appropriate.

[1] BlackRock

[2] Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA.

[3] J.P. Morgan Asset Management

[4] University of Michigan

[5] Federal Reserve Bank of St. Louis

[6] MarketWatch