Steady Markets, Split Economy

4Q 2025

By Cliff Aque, CFA

The fourth quarter of 2025 put a bow on a year that looked chaotic in headlines but coherent in markets. Growth held together, inflation cooled without collapsing demand, and financial markets did what they tend to do when uncertainty fades just enough: they climbed. By year-end, most major risk assets were higher, volatility was lower, and investor pessimism—abundant earlier in the year—quietly receded.

The economic story entering Q4 was one of moderation rather than contraction. Labor markets cooled but did not break. Job openings declined, hiring slowed, and wage growth normalized, yet consumer spending remained resilient. High-income households continued to benefit from strong balance sheets, asset appreciation, and stable cash flow. Lower-income households, however, remained under pressure from the combined effects of higher prices and the lagged impact of higher interest rates.

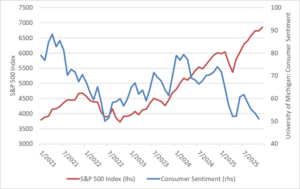

This divergence has contributed to what is increasingly described as a K-shaped economy, where outcomes for higher- and lower-income consumers continue to move in opposite directions. A similar pattern has emerged in the corporate landscape. Mega-cap companies have maintained stronger earnings growth and more flexible cost structures, aided by lower leverage and a greater share of fixed-rate debt issued prior to the rise in interest rates. The chart below highlights this divergence, as broad measures of consumer sentiment remain historically subdued even as equity markets reached new highs.[1].

Inflation continued to trend down for the most part, but it has been uneven. Goods inflation continued to fade and shelter pressures slowly rolled over; however, services inflation proved more persistent. The Federal Reserve responded with a more accommodative posture in the second half of the year, reinforcing market confidence that monetary policy was no longer actively restraining growth. Fixed income markets responded favorably, delivering positive returns while still offering yields that remain attractive by post-financial crisis standards.

Equity markets, however, were the headline act. U.S. equities again delivered solid gains, though leadership remained concentrated. Large-cap growth—particularly companies tied to artificial intelligence, infrastructure build-out, and productivity enhancements—continued to command capital. Outside the U.S., equity performance broadened meaningfully. International developed and emerging market stocks benefited from improving growth expectations and, importantly, a weakening U.S. dollar.

Dollar weakness is a double-edged sword. For U.S.-based investors, it enhances returns from non-U.S. assets and supports multinational earnings growth. At the same time, it can reintroduce inflationary pressure by raising import costs and loosening financial conditions. That tension bears watching, particularly as fiscal policy remains expansionary.

On that front, fiscal stimulus remains a defining variable heading into 2026. Programs tied to infrastructure, industrial policy, and deregulation—including components of the OBBBA—are supporting nominal growth. That backdrop is constructive for earnings and risk assets in the near term. However, layered onto a labor market that may be tighter than headline figures imply, it increases the risk that inflation proves stickier than markets currently expect. This is not a call for runaway inflation, but rather a reminder that disinflation rarely moves in straight lines.

Fixed income markets reflected this balance of optimism and caution. Yield curves steepened modestly as growth expectations stabilized, and credit spreads remained tight. Bonds once again played their intended role: income generation with ballast—not a home run asset class, but a reliable one. Alternatives, particularly real assets, continued to serve as measured hedges against geopolitical and fiscal uncertainty.

As we move into 2026, the base case remains positive. Earnings growth is expected to broaden beyond mega-cap stocks, financial conditions remain supportive, and global diversification will hopefully continue to be rewarded. However, risks are no longer theoretical. A sharper labor market slowdown could challenge consumption, while persistent fiscal stimulus and dollar weakness could slow the final leg of the inflation fight. Neither outcome necessarily derails markets—but both increase the chances of a pullback.

For high-net-worth investors, this environment reinforces a familiar discipline: stay invested, diversify intentionally, and resist the urge to chase yesterday’s winners. The opportunity set remains attractive—but selectivity matters more than enthusiasm. In markets like these, steady often outperforms flashy. Boring, once again, may turn out to be beautiful.

[1] Source: S&P Dow Jones Indices LLC; University of Michigan via FRED®. You cannot invest directly in an index.