Reaching New Heights

3Q 2024

The S&P 500 Index, a key indicator of the overall stock market, reached 43 new all-time highs in 2024, with the latest at 5,672 at the end of Q3 and the previous on July 16th at 5,667. The market had been rising steadily until mid-July, when weak reports from major S&P 500 stocks, a surprise rate hike from Japan, and labor market concerns unsettled investors. Volatility spiked in August but soon receded as strong earnings, moderating inflation, and a 50-basis point rate cut from the Federal Reserve stabilized sentiment.

By Q3’s end, the top 10 S&P 500 stocks accounted for over one-third of its market cap, an unusually high level, driven by strong earnings growth and global investor interest. A popular strategy was borrowing against the low-yield Japanese yen to invest in high-growth U.S. tech stocks. However, as tech earnings faltered and Japan announced a rate hike on July 31st, the “Japanese carry trade” rapidly unwound. Fears eased through August, leading to the 43rd all-time high in late September, with increased participation from stocks outside the top 10.

Market confidence further improved after the Fed’s “jumbo” rate cut of 50 basis points on September 18th. Though large cuts often signal negative events, Fed Chair Jerome Powell framed it as a proactive step to support the economy. With inflation declining without recessionary pressure and perceived labor market weakness, the Fed saw room for a larger cut. However, the strong September jobs report, showing 254,000 new jobs vs. a 150,000 forecast, raised questions about whether it was too much, too soon.

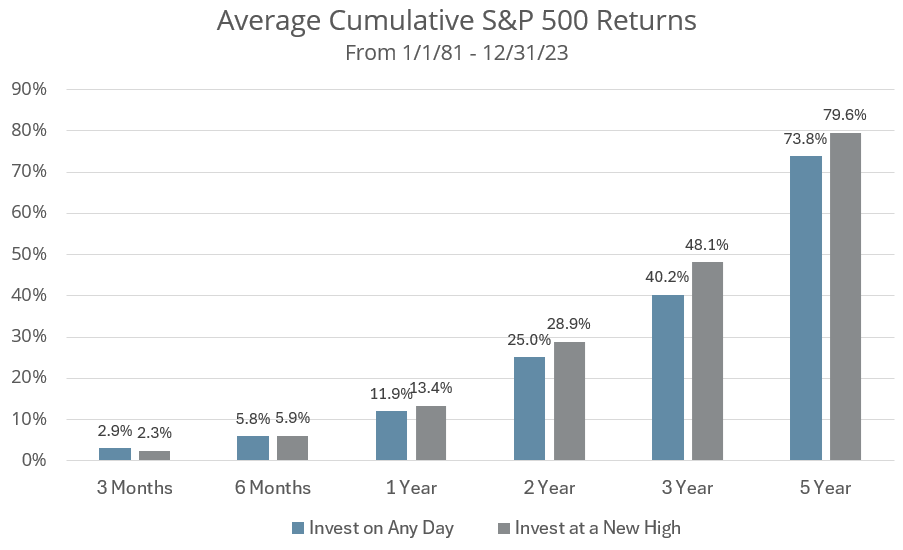

Given the strong corporate earnings, easing inflation, and a resilient job market, the economy appears well-positioned for a soft landing. This brings us back to the media’s focus on “all-time highs,” which can deter some investors. But reaching new highs is exactly what markets are supposed to do. From 1988 to 2023, long-term investors have generally performed better when investing at market peaks, as strength tends to follow strength.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management

The reason for this outperformance is that market highs tend to be clustered together as market strength leads to more market strength. Market highs shouldn’t be a reason to stay on the sidelines. While valuations may seem elevated due to larger S&P 500 stocks1, an equal-weighted index shows that they are closer to historical norms. With a solid economic backdrop, growing earnings could continue to propel the market higher.

As 2024 draws to a close, uncertainties remain—Russia/Ukraine, Middle East tensions, China/Taiwan, and U.S. political risks—but over the long term, these issues have little impact on the market’s trajectory. Investors should focus less on geopolitics, elections (the topic of our upcoming webinar), or record highs, and more on the underlying fundamentals.

[1] Investors cannot invest directly in an index.