Spring Is Here?

By Tim Egart, CFP®, AIF®

Major League Baseball celebrates Opening day for their 2021 season on April 1st. To me, Opening Day is a milestone that suggests the dreariness of winter is ending and spring is finally here. Opening Day is the precursor to days of sunshine, of catch in the front yard with my boys, of a fishing line in a pond, or of a pool party with family and friends.

But even as we look towards the sunny, 75-degree days ahead, we continue to dig ourselves out of the economic winter that COVID-19 has caused. Fortunately, some rays of sunshine have finally begun peeking through.

COVID-19 Vaccinations & the Path to Immunity

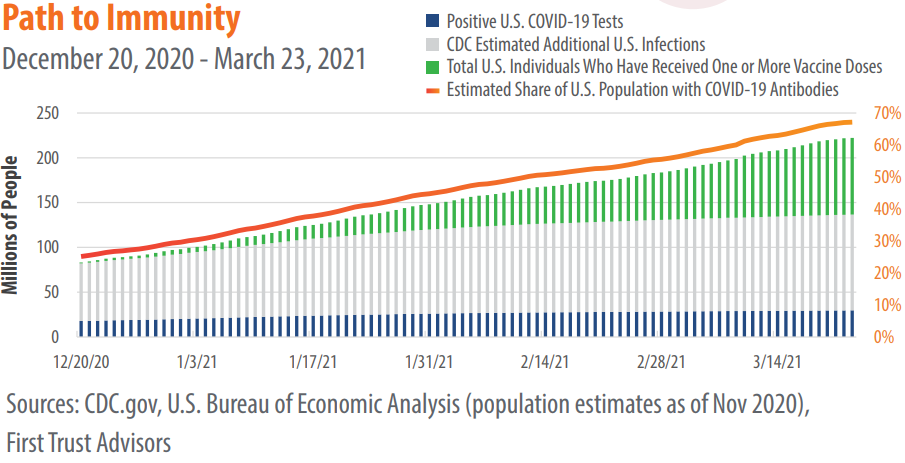

The United States continues to progress towards mass vaccination with nearly 146 million vaccine doses administered, per Bloomberg.[1] In the span of 15 months, we have identified a virus, created multiple vaccines for said virus, mass-produced these vaccines, and administered vaccinations to millions of people. As we expand vaccinations to include the general population, the percentage of people who are believed to have established immunity continues to increase.

While the exact path to herd immunity can be debated another time, our current pace puts us at approximately 68%, as shown by the chart below:

Company Earnings

Economist Ben Graham famously said that “in the short run, the market is a voting machine but in the long run, it is a weighing machine.” Myriad factors can move the market in the short term: interest rates, trade wars, vaccine development, Fed policy, and so on. But in the long run, the market’s performance comes down to company earnings: how much profit did a company deliver to its bottom line?

For Q4 ’20, JP Morgan estimates year over year earnings per share will be down roughly 2.7% year over year vs. Q4 ‘19 for the S&P 500.[2] Digging deeper into this, there were winners (technology and healthcare) and losers (financials, energy, industrial companies). As we see localities, states, and countries continue the path towards resuming normal operations, there is a renewed expectation for revenue/profit expansion among the former “losers.”

Fiscal & Monetary Stimulus

The Fed has pumped the brakes on expanding the money supply in recent years, but that changed last year. Shortly after the COVID crisis began in earnest, the Fed significantly expanded the money supply, and today, the money supply is 27% higher than it was a year ago.[3]

With interest rates sitting near zero (but slowly climbing) and the world awash with cash, the calculus has moderately changed for measuring risk. Right or wrong, these monetary conditions have effectively encouraged investors to move money into stocks.

Unlike much of what we’ve seen from lawmakers over the past decade or so, Congress has also decided to get in on the act, passing massive fiscal legislation to bolster consumer finances and business liquidity moving forward. In addition to the CARES Act and HEROES Act, Congress also passed the American Rescue Plan on March 11th, releasing another $1.9 trillion in stimulus funds.

These easy money and stimulative actions taken by the Fed and Congress can lead to higher asset prices — at least in the short term.

Overall, there are undoubtedly glimmers of sunshine in the market and the economy, but a spring storm is not out of the question. Like any market season, there are a number of potential events that could lead to additional volatility: a setback in our efforts to get COVID under control, inflation, debt levels, and so on.

Throughout history, the S&P 500 averages a decline of ~14% from peak to trough in any given year, which suggests that it might be more surprising if we don’t see some volatility in the months ahead.[2] But if or when it occurs, we’ll be here to help you navigate it. As the saying goes, “April showers bring May flowers.”

[1] Bloomberg, Covid-19 Vaccine Tracker.

[2] JP Morgan, Economic Update: March 15, 2021.

[3] Trading Economics, United States Money Supply M2.