The Fed’s Influence on Markets

By Damaris Gingerich, CFP®, AIF®

What does the Fed do?

The Federal Open Market Committee (FOMC) has a two-part mandate: control inflation and achieve maximum employment. Their stated target is 2% inflation with maximized employment. The Committee is comprised of 12 members, headed up by Fed Chair Jerome Powell, who began his term in 2018.

Source: Federal Reserve Bank of Chicago

The FOMC meets at least eight times a year and meeting minutes are released for the public afterwards. They have a few powerful tools with which to accomplish their objectives: setting reserve bank requirements (how much cash that banks must hold in reserve), changing the discount rate (interest charged by the Federal Reserve to financial institutions for short-term loans), and buying or selling government securities to the public.

What has the Fed been trying to achieve recently?

In recent years, as always, the FOMC has been working on both parts of their mandate. Most of us felt the effects of COVID-19 in 2020, particularly in the job markets as unemployment moved from 3.5% to 14.7% in April of 2020.1

In response to a weakening economy, the Fed used its tools to ease monetary policy. This included buying government securities from the public (to increase the supply cash) and promising to keep interest rates low until the FOMC felt confident in economic recovery (to make borrowing easier). These actions among others helped to mitigate damage to the economy resulting from the pandemic.

Source: discover.com

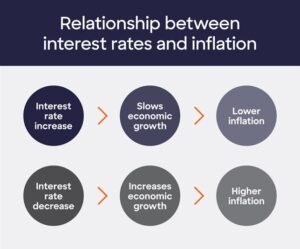

The US economy recovered quickly from COVID, in large part due to stimulus payments for individuals and supportive policies for businesses. However, this also led to an increase in the nation’s money supply. Prices of goods and services crept up while consumer spending remained strong. Soon the Fed was worrying about higher inflation. This time, the Fed used its tools to tighten monetary policy by raising interest rates. In 2023, the goal was that gradual rate increases might stave off inflation without slowing the economy to such a degree that a recession would be triggered.

In large part, the Fed has progressed toward the “soft landing” they were aiming for. Investment markets have continued to reach new highs and jobs have remained relatively stable through the first two quarters of 2024. Initially this year, the market had (errantly) priced in the expectation for several interest rate cuts beginning as early as March. But inflation has remained elevated, and the Federal Open Market Committee has been firm in their desire to see progress against inflation before implementing any interest rate cuts. More recently, jobs data has indicated that unemployment may also be creeping up.

Reports from the month of April were telling. The prices that businesses pay for goods and services, as measured by the Producer Price Index, data evidenced hotter inflation, while the Consumer Price Index revealed moderating inflation. Most recently, May data revealed that while expectations for the Producer Price Index were a .1% increase, prices fell .2%.2 The Federal Reserve wants to see more evidence of cooling inflation before making a cut to interest rates. The idea of rate cuts starting in the Spring is long gone and September now seems more likely. More recently, unemployment ticked up modestly in May to 4% after 27 consecutive months below 4%, which was the longest streak since the late 1960s.3

What do jobs have to do with interest rates?

Since unemployment is so important to the Fed’s dual mandate, each employment report can provide indicators about employment as a sign for the Fed regarding their best course of action.

Source: educba.com

To sum up, US equity markets respond favorably to the expectation of increased money supply and the expectation of low interest rates for borrowers. While the Fed seems to be in a holding pattern currently, the markets expect interest rate cuts on the horizon that will open up the economy and increase consumer and business spending. For the long-term investor, we’d advise against trying to guess what the Fed will do. They have a poor record of living up to their own forecasts and that trend will likely persist in the face of future data.

1 What did the Fed do in response to the COVID-19 crisis?