The First “Correction” Since 2011

3Q 2015

When the stock market gets volatile, it’s sometimes hard to decipher what is real. But let’s be totally honest – US economic data (especially the domestic side of it – consumer spending, housing, auto sales, employment, and inflation) is doing well. However, our markets are being dragged down by foreign market developments. In times like these, it’s important to keep some perspective. Yes, the S&P 500 was down 6.9% in the third quarter (-6.4% when including dividends), but very little of that pullback was attributable to our own economy. Most was connected to fears that emerging markets were decelerating. Let’s recap.

After a cliffhanger of a second quarter, with Chinese markets beginning a late-June swoon and Greece officially missing its IMF payment, the third quarter looked to be continuing down a bad path. However, within a couple of weeks the Greek government realized the error of its ways and accepted austerity terms that were even more harsh than the ones the populace had recently rejected in a public referendum. It looked like contracts would be honored and order would be restored as global markets turned around and were back on their way higher.

That was until a couple weeks later when emerging markets refused to cooperate. Manufacturing figures out of China began to turn slightly more negative, which further exacerbated a slide in commodity prices. The thought was that if demand from one of the largest consumers of commodities in the last decade or so (China – for use in building infrastructure, manufacturing facilities, condos, etc.) was slowing down, commodity prices might be under pressure for a while. With many emerging countries heavily reliant on the sale of commodities, emerging market stocks were -17.8% in the quarter. That compared to other foreign developed market stocks which were -10.2% in the quarter.

Adding to the anxiety in the market was uncertainty as to when the Federal Reserve would raise interest rates (for the first time since June 2006). The media focus on the September meeting was intense, complete with countdown clocks for the announcement. When the Fed announced they would not raise rates, traders became nervous, concerned that the global economy was just too fragile to withstand higher US rates. But let’s keep the last Fed meeting in perspective. Will it really matter one year, or five years, or 10 years from now that the Fed chose to raise or not raise interest rates at the September 2015 meeting? It won’t. It’s the long-term that really matters.

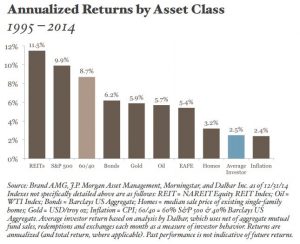

In the end, many investors had become complacent in recent quarters with what they thought was an endless march higher for stocks (remember: a risky asset class, which brings with it the potential for higher long-term returns). This had caused some to abandon diversification and increase their allocation to stocks. That all changed in late August, when those caught with too much stock exposure had to quickly reduce it, and those who remained truly diversified were helped by their bonds – the Barclays Aggregate Bond Index finished the quarter +1.2%.

All of this “noise” makes for opportunity. It always does. This is a season where disciplined re-balancing and disciplined tax loss harvesting (where applicable) yield their fruit. These are steps that are never easy but they are important. We surely acknowledge that simple words like “China” or “Yellen” or “Jobs” can swing investor emotions and markets more than we expect. This is the wired world we live in. For you, at the individual, family or corporate level, our encouragement remains the same: keep going. This has been a bit of an overdue correction and it has not diminished our intermediate to long-term convictions at all. We hope the same for you.