The Old Normal

2Q 2024

By Cliff Aque, AIF®, CFA®

During the Great Financial Crisis (GFC), the phrase “the new normal” gained popularity. However, it has also been used at other times of dilemma: in 1918 regarding the aftermath of World War I, in 2003 after the dot-com bubble, and in 2005 during the avian flu (according to Wikipedia). There is always a new normal, but perhaps we are returning to an old normal of higher delinquencies, higher unemployment, higher inflation, and higher interest rates. Since these are rising from historic lows, this might not be such a bad thing.

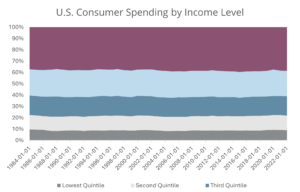

The U.S. economy is still doing fine, driven by a strong consumer base. While higher delinquencies have shown some weakness, as mentioned in our fourth-quarter 2023 commentary, they appear to be leveling out at pre-GFC and pre-COVID levels. Importantly, these delinquencies tend to affect lower-income earners, while higher-income earners are less impacted by rising rates and can more easily absorb price increases. As shown in the chart below, the highest quintile of income earners consistently spends as much as the bottom three quintiles combined. For example, TSA checkpoint travel numbers set a record high on July 7th, with over three million passengers for the first time ever, and flying is a highly discretionary consumer spending item.[1]

Source: Brand AMG, St.Louis Federal Reserve (FRED), U.S. Bureau of Labor Statistics.

There has also been some weakness in employment numbers, with June data showing unemployment rising to 4.1% from its earlier low of 3.6% this year. Additionally, job creation was below expectations, with 200,000 jobs created. Although the number of jobs being created has steadily decreased over the past three years, this trend is skewed by the millions of jobs lost during COVID. Looking further back, 200,000 jobs created is an average number for any period. 4.1% unemployment is still historically low considering that it has averaged 6.2% over the past 50 years. Wage growth has also slowed to 4%, but is still above the 50-year average of 3.9%.

Inflation continues to moderate, with headline CPI at 3% in June, mostly due to falling energy prices. However, shelter and insurance premiums, which are stickier components, continue to contribute to CPI. While the Fed may have won this recent battle with inflation, history shows that inflation is a long-term issue and can reignite. After World War II and in the 1970s, inflation surged back after being initially contained—twice. Although our current economic situation is different, we should be prepared for inflation above 2%.

Regarding interest rates, since the Fed first started publishing the Fed Funds rate in July 1954, it has averaged 4.6%. The Federal Reserve Open Market Committee’s long-run projection for rates is 2.8%, higher than any time since the GFC but still lower than the old normal. With recent job and inflation numbers, the Fed might cut rates in September and possibly in December, but only time will tell.

Finally, with the stock market hitting all-time highs and the hype around artificial intelligence, there are concerns about market valuations. Some companies do appear overvalued, and the markets are higher mostly due to a few names. In the second quarter, the top five names in the S&P 500 accounted for 110% of the overall index return, and the top ten accounted for 123%[2]. This premium distorts the broader market’s valuation. Looking at an equally weighted S&P 500 benchmark, the average next-twelve-months price-to-earnings ratio is 15.8x, slightly above the old normal average.

The markets are likely to remain volatile with the upcoming election and geopolitical noise, but the economy remains healthy with many good investment options. We continue to emphasize diversification, rebalancing between winners and losers, and maintaining a long-term view. Returning to the old normal might make life harder than during the last “new normal,” but it could lead to an even better place.

[1] Source: https://www.tsa.gov/travel/passenger-volumes

[2] Investors cannot invest directly in an index.