The Times They Are A-Changin’

2Q 2017

The Greek philosopher Heraclitus is quoted as saying “change is the only constant in life.” Changes, like most things, come in different varieties. Some are small, fast changes; others are large, slow changes. Markets are famous for giving investors daily (even hourly) small, fast changes. But these days, we may be witnessing some of the large, slow variety.

One example of this can be seen in the shift of global central bank policies. Nearly a decade ago, governments and central banks around the world reacted to the global financial crisis of 2008. In the US, the Federal Reserve Bank began QE (quantitative easing) which saw the size of the bank’s balance sheet grow from about $800 billion in the fall of 2008 to about $4.5 trillion today. Fast forward to today, where the Federal Reserve announced that they would soon begin the process of unwinding (aka reducing the size of) their balance sheet, marking the beginning of a long road back to “normal”. Other central banks around the world are similarly hinting at changes to their post-crisis accommodation, as the needs for such policies are no longer that great.

Central bank policy shifts are akin to turning a steamship around. They require a small, yet steady, turn of the wheel and can take a long time to complete. Once the process has begun, however, the change in policy trajectory will have ripple effects for other markets. Some of those ripple effects can be anticipated, but there are many other implications that no one yet knows.

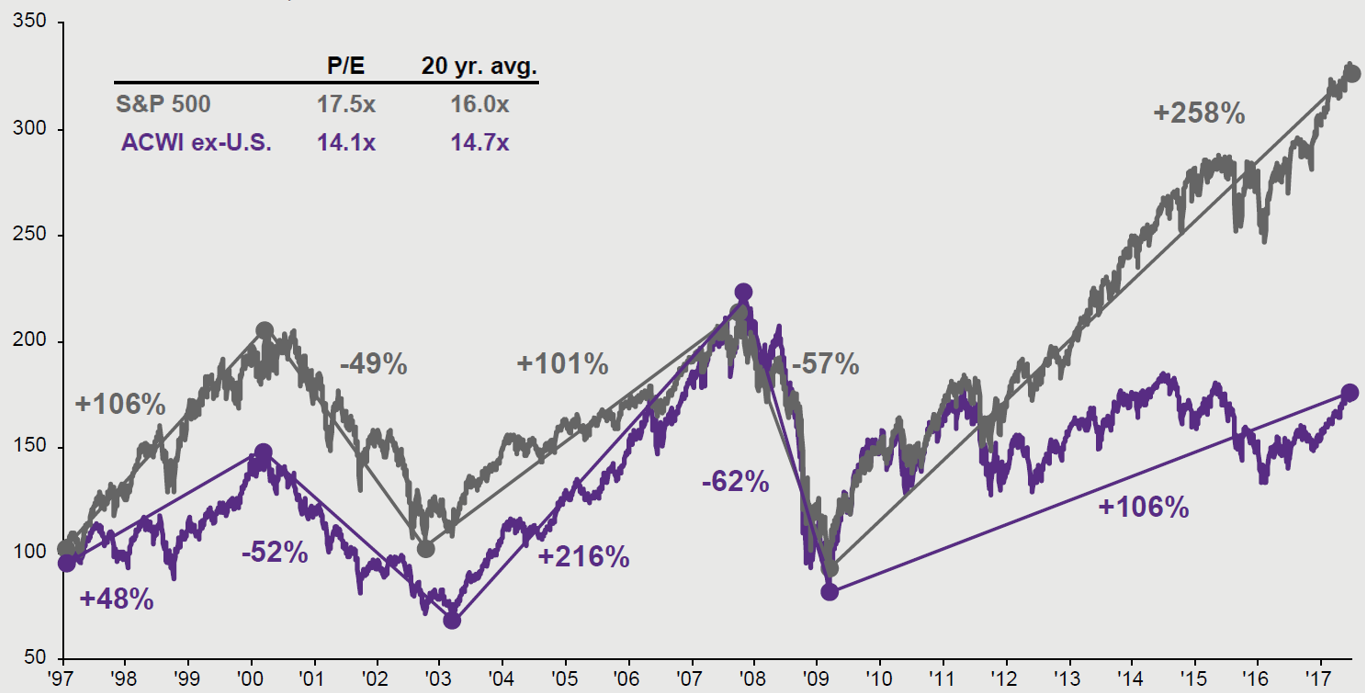

Another example of a potentially large and slow change can be seen in regional market leadership. Since the financial crisis, the US stock market (as measured by the S&P 500) is up 258%. In contrast, “foreign” stock markets (as measured by the MSCI All Country World ex-US index) are up only 106%. On a calendar year basis, the US market has outperformed international markets in six of the last seven years. However, foreign markets are recently beginning to gain traction in economic growth, the likes of which have not been seen since 2011. As international fundamentals improve, globally diversified investors are once again being rewarded, with international large cap stocks outperforming US large cap stocks 14.2% to 9.3%, respectively, year-to-date on a total return (including dividends) basis.

For investors, this is good news given that the US stock market continues to trade at a “slightly-expensive” valuation and the bond market continues to face the prospect of eventually-higher interest rates (one of the ripple effects previously alluded to, and one which temporarily reduces returns to bond investors). With international markets still trading at a discount to their long-term average valuations, the budding improvement in fundamentals affords international investors even better opportunities in the form of additional upside.

We don’t pretend to be able to predict which markets will outperform. But, what we know is that maintaining proper diversification (in stocks, bonds and the right alternatives) and being ready to rebalance where appropriate results in better long-term performance for investors. The fact is, markets can stay “expensive” for long periods. Alternatively, faster economic growth (in any area of the world) can help balance markets and even allow expensive markets to “grow into their valuation”. We are glad to see better growth in Europe and other non-US areas, and welcome the stability this change may provide to properly diversified portfolios.

MSCOI All Country World (ex US) versus S&P 500 Index

Source: MSCI, Standard & Poor’s, FactSet, J.P. Morgan Asset Management. Data as of 6/30/17. December 1996 = 100, U.S. dollars, price return. Forward P/E ratio is a bottom-up calculation based on the most recent index price, divided by consensus estimates for earnings in the next twelve months (NTM), and is provided by FactSet Market Aggregates. Returns are cumulative and based on price movement only, and do not include the reinvestment of dividends. Past performance is not indicative of future returns.