2015 – The Year That Barely Happened

4Q 2015

The S&P 500 finished the year up a paltry 1.4% on a total return basis (including dividends), but was down 0.7% on a price-only basis (excluding dividends). For anyone who fell asleep at the beginning of the year and woke up on December 31st, it sure would have seemed (by looking at most market levels) that nothing happened. But nothing could be further from the truth. During the year the world endured multiple terrorist attacks, an escalation to the Syrian civil war and other Middle East conflicts that caused a global refugee crisis, collapsing commodity prices, massive volatility in the Chinese stock market, the first US market correction since 2011, the first Federal Reserve rate hike since 2006 (which finally occurred after multiple head-fakes), continued softness in oil prices (which kept world markets nervous) and a high yield bond scare.

So how did it shake out? Shortly after the calendar turned to 2015, stocks in the US leveled off from their three-year ascent. For most of the first half of the year, stocks were pretty much unchanged. As summer set in, a large drop in Chinese markets triggered a correction in the US. For the remainder of the year, global markets did their best to heal in the face of a strong dollar, falling commodity prices, and the inevitability of the dreaded Fed rate hike. The fact that most markets (excluding emerging markets and international small cap stocks) finished relatively “neutral” for the full year is quite a feat given the hole that had been dug for investors in the third quarter.

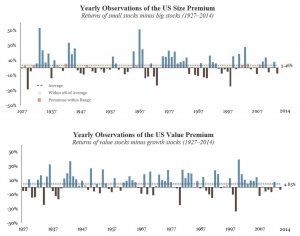

For the second year in a row, large cap stocks outperformed small cap stocks, and for the ninth quarter out of the last ten, growth stocks outperformed value stocks. Long-time clients of BAMG know that this outcome runs counter to the decades-old academic research which shows that over longer periods of time, small caps outperform large caps (by an average of 3.5% per year) and value stocks outperform growth stocks (by an average of 4.9% per year).

We appear to be in the midst of one of those short-term aberrations which tend to happen from time to time. As such, the way we construct portfolios (with a “tilt” toward small caps and value) produced a slight headwind to overall performance.

With interest rates still near historic lows, but poised to rise at some point, returns for bonds may be somewhat muted in the intermediate term. Ultimately, the speed and magnitude of any interest rate increase will determine how bonds fare. However, it’s important to remember that bonds play the essential role of stabilizer (especially during times of equity volatility) and risk-reducer in a portfolio. High yields bonds experienced a decline late in the year associated with low oil prices and the closure of one very risky high yield bond fund. However, that sell-off and the fact that emerging market bonds are holding up well have many analysts declaring that high yield bonds are now very inexpensive.

In periods of volatility, we remain resolute, and know that the greatest value we serve is in helping clients remain disciplined. When most investors were scared in the third quarter, we re-balanced to enhance long-term returns. Where applicable, we harvested tax losses to help clients minimize their tax bills. All along, we avoided chasing “higher yields” in the high yield bond space because “higher yields” generally come with lower credit ratings and greater volatility. We do these things, because even during periods when it seems like the markets are going nowhere, all the little things (blocking and tackling) add up to big things in the end.