Trade War Fireworks

2Q 2019

All in all, the second quarter turned out to be a good one for stocks. The S&P 500 was up 4.3% on a total return basis (including dividends), but it wasn’t easy getting there. The index initially continued its first quarter run higher, eventually setting a new high on May 3rd thanks to a first quarter earnings season that topped analysts’ tempered expectations, as well as a general feeling that the US and China were nearing a trade compromise.

However, in early May, President Trump turned up the heat on trade negotiations by raising Chinese tariffs from 10% to 25% and threatening to impose tariffs on the remaining balance of Chinese imports. This resulted in a volatility aftershock from the fourth quarter, with the S&P falling 6.8% over the next four weeks. Market conditions would stabilize in June as Federal Reserve officials floated the idea of lowering interest rates to help buffer any slowdown that might be caused by trade frictions, helping stocks recover over the next four weeks.

International developed market stocks moved roughly in tandem with US stocks, but emerging market stocks trailed other global markets due to its larger weight represented by China – the chief target in the US’s trade war dispute. All the while, interest rates moved much lower keying off the Fed’s hint of rate cuts. While the ten-year US Treasury bond opened the quarter at 2.49%, it finished the quarter at 2.00%. This allowed bonds to post a much better return than they otherwise would have (when rates fall, bond prices rise), with the US Aggregate Bond Index finishing +3.1%.

As we officially begin the longest economic expansion in US history (as of July 1st), we are reminded of all the things that were supposed to derail it over the years: fiscal cliffs, Meredith Whitney’s 2010 prediction of “50 to 100 sizable defaults” in the U.S. municipal market totaling “hundreds of billions of dollars”, Russia invading Ukraine, ISIS, the “Arab Spring”, Greece defaulting on its debt and leaving the Euro, Brexit, the Fed unwinding Quantitative Easing, European debt problems, Chinese debt problems, the election of President Trump, and nuclear war with North Korea (just to name a few).

Some investors worry that the expansion is running out of time, but an old adage notes that “bull markets don’t die of old age” – and we agree. Length of an expansion has no direct correlation to its ultimate duration. Instead, it is based on economic fundamentals, which are still in expansion territory (albeit slowing).

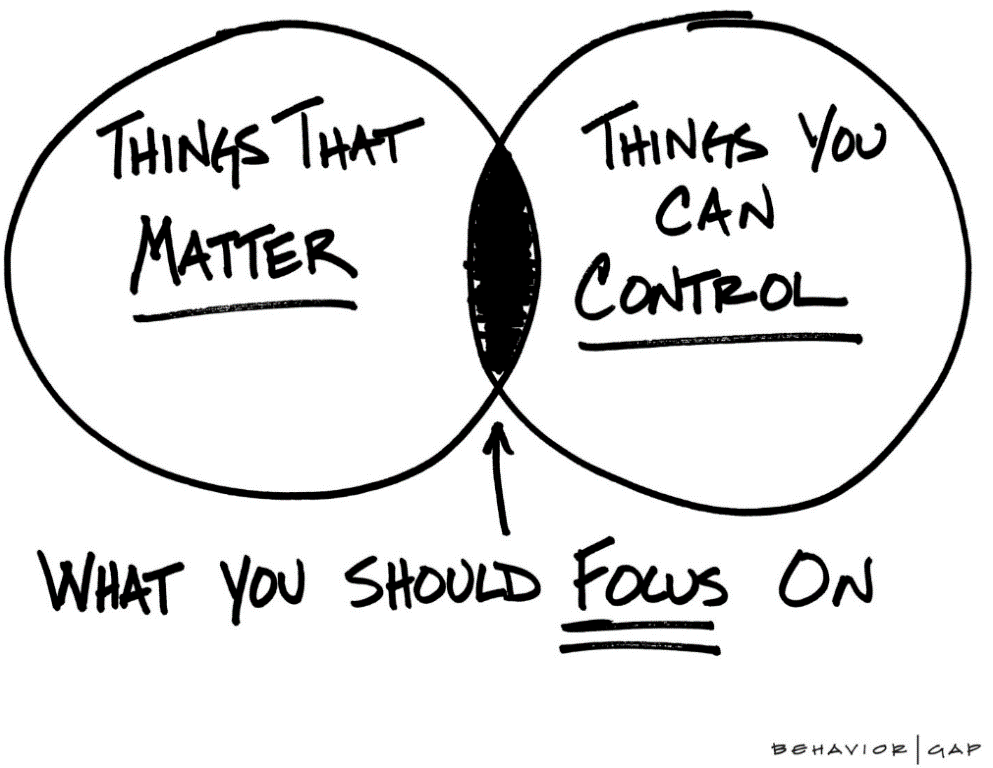

We imagine that over the next few months and quarters, especially as we start to enter a new presidential election season, we may see more rhetoric about the economy, trade and geopolitics. It will be important for us as investors to recognize that we cannot control market and economic events, but we can control our reactions to the volatility that inevitably occurs around those events.

That said, it is always wise to remain focused on what we can control (staying invested and diversified, not trying to time the market, rebalancing when and where appropriate) – and not on what we can’t.