Trade War Tremors

Market days like the one we had yesterday can be scary. At its low point, the S&P 500 was down 3.7%; the equivalent of a 993 point drop in the Dow Jones Industrial Average. It was the first time we’ve had a drop of 2.5% or more in a day since the fourth quarter of 2018.

Back then, though, you’ll recall we had three days where the S&P fell more than 3%. The market ultimately traded down 19.8% from it’s most recent high, but everyone knows what happened next: the Fed began to talk about more accommodation and trade threats began to ease. A day after putting in its bottom, the market was up 5.0%.

This reminded us that the best up days are usually within a few days of the worst days, making market timing twice as difficult: investors experience the pain and “go to cash”, only to miss the ensuing rebound! By April 23rd (roughly four months later) the S&P was at a new all-time high.

What is different about this time is that we don’t (yet) have hindsight in our favor – no one knows how this volatility will play out. What we do know is that it seems like every time the US-China trade war rhetoric heats up, the markets become volatile.

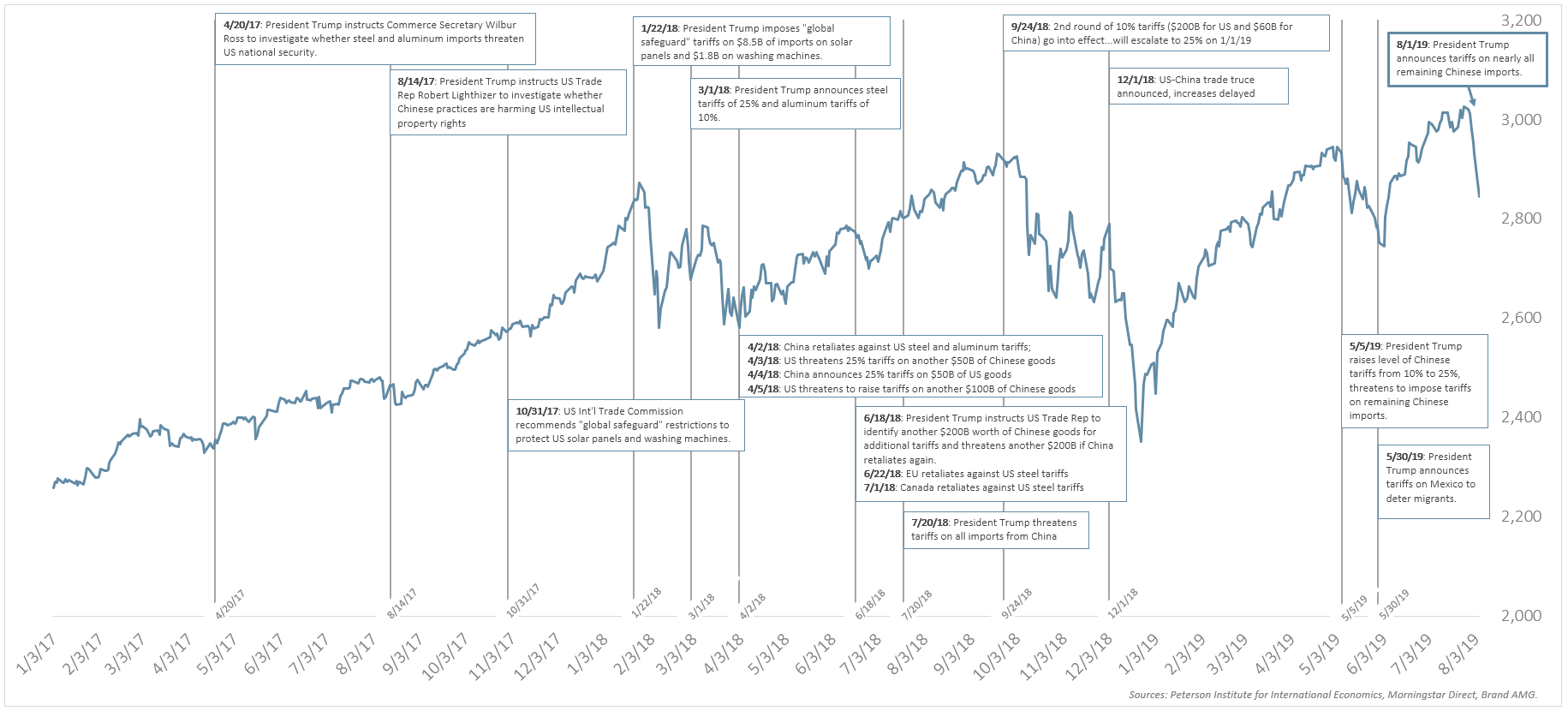

S&P 500 amidst the trade war – timeline of events through August 5, 2019

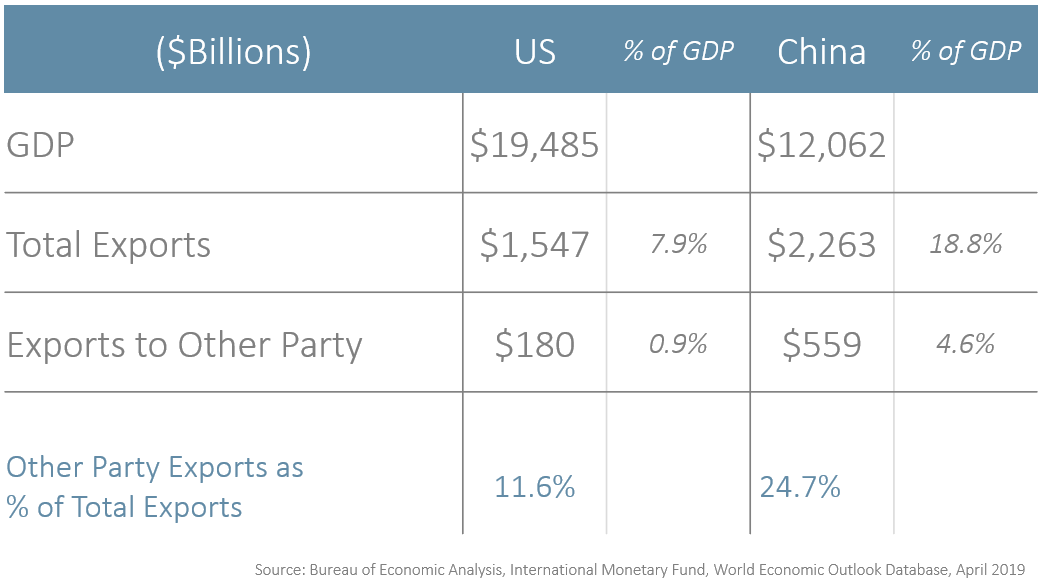

We believe that the trade dispute seems to be less about trade per se, and more about technology – particularly about the protection of US intellectual property, as well as control over future technology standards. And we know that this feud has a far bigger impact on China than it does the US. Total exports represent 18.8% of Chinese GDP, more than double that of the US – only at 7.9% of our GDP comes from exports.

Furthermore, 24.7% of all Chinese exports are to the US, which is again more than double the US figure (11.6% of total US exports go to China). These figures (also shown in the chart below) provide tremendous context for which party has the most leverage in this dispute.

US – China Trade Summary

We are strong believers that free trade makes everyone better off (see link below to a parody video that does a great job explaining the benefits), and while we hate to see threats to global trade result in market volatility, we believe that eventually, a ceasefire will occur that results in better protections for US companies and the technological progress that we bring to the world. When will that truce occur? Nobody knows for sure – but there’s another election coming up soon, and incumbents do better when the economy is strong. However, trying to time it just right can certainly end up being a costly gamble.

In the meantime, the US economy still appears to be doing fine (albeit exhibiting some deceleration), with nonfarm payrolls adding 164,000 jobs in July, core retail sales +4.4% year over year in June (recall the consumer is ~70% of US GDP), and core inflation of 2.1% in June, which is close to the Fed’s 2% target.

We encourage investors to use volatile opportunities like this to rebalance where appropriate to attempt to improve longer-term returns.