When the Road Map Changes

1Q 2026

By Cliff Aque, CFA

Markets entered 2026 with the wind at their backs: a growing economy, cooling inflation, three Fed rate cuts, and five consecutive years of double-digit earnings growth. Then the road map changed. By the end of the first quarter, the S&P 500 had declined 4.3%[1], with tech stocks hit significantly harder. Three forces converged to reshape the quarter: renewed questions about AI capital spending and whether it can deliver commensurate returns; a Supreme Court ruling that forced a reset of the tariff structure; and a sharp escalation of conflict in the Middle East that drove oil prices to levels that put the Fed in a difficult position. The markets aren’t broken, but the easy part—riding momentum and favorable macro tailwinds—is behind us. The harder work of differentiated returns is ahead.

The first crack came from technology. During fourth-quarter earnings season, investors began asking when the hundreds of billions of dollars committed to AI infrastructure by the largest tech companies will generate returns. Meanwhile, software-as-a-service stocks fell sharply as new AI capabilities raised questions about pricing power and competitive moats. U.S. software stocks declined roughly 24% during the quarter.[2]

The second development was legal. In February, the Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA), the authority the administration had used to impose sweeping “reciprocal” tariffs in 2025, did not provide a valid basis for those tariffs. The administration responded by implementing a flat 10% tariff on all imports. That uniform rate is not what businesses hoped for, but for markets, certainty about the rules tends to matter more than the level of the rules.

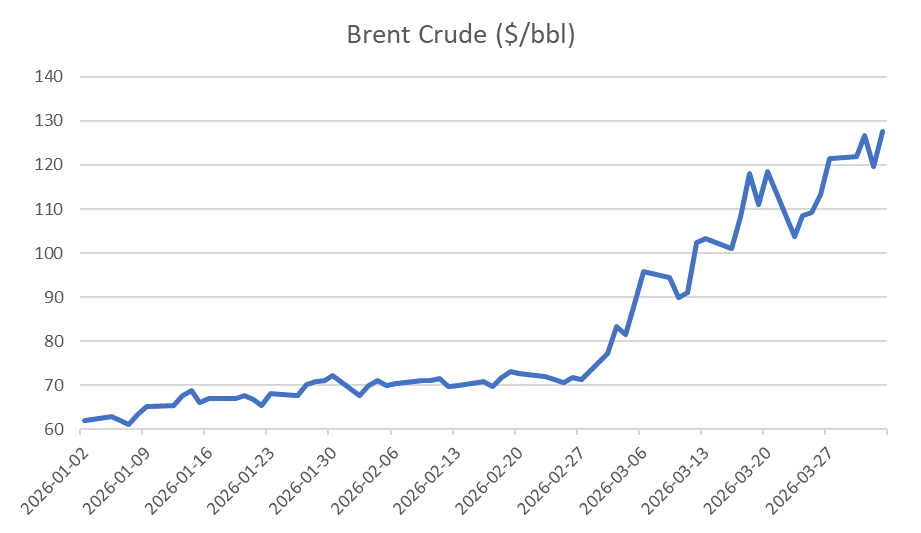

The third and most significant event was the escalation of conflict in the Middle East. The Strait of Hormuz, through which roughly 80% of global oil and gas destined for Asia transits[3], became a focal point for supply disruption. Brent crude, which had been trading below $65 at the start of the year, hit a record high of $144 per barrel on April 7th prior to the two-week cease fire announcement.[4] For a global economy that had spent two years normalizing inflation, a commodity price shock of this magnitude was unwelcome, and for the Federal Reserve, presents a problem.

Source: U.S. Energy Information Administration via FRED®.

There is no elegant solution when the economy is simultaneously facing an inflationary supply shock and a slowing labor market. At its March meeting, the FOMC left the federal funds rate unchanged at 3.50–3.75%, and Fed Chair Powell described the labor market as a “low-firing, low-hiring environment.” [5] February payrolls shrank by 92,000 against expectations for a 60,000 increase.[6] Meanwhile, oil prices were pushing inflation back above 3%.

This already difficult balancing act takes place against an unusual backdrop. Kevin Warsh has been nominated to succeed Jerome Powell as Fed Chair, with his first meeting expected in June. The administration has been vocal about its preference for lower rates. That creates a dynamic worth watching. Markets will be scrutinizing the transition not just for policy signals, but for signals about whether the Fed’s independence remains intact.

Lost in the noise of geopolitics and Fed watching is that corporate earnings have been quite good. The S&P 500 is on track to report approximately 13.2% year-over-year earnings growth for the first quarter—the sixth consecutive quarter of double-digit growth.[7] The market sold off not because fundamentals deteriorated, but because sentiment rotated, geopolitics introduced a new risk premium, and valuations in certain areas—particularly mega-cap tech—were priced to perfection and left no room for uncertainty.

We believe two issues will shape the remainder of 2026 in ways that will not be resolved by the next payroll report. AI must move from narrative to evidence—investors need to see whether the massive capital commitments made by the largest technology companies translate into sustainable earnings growth, or whether the spending itself was the story. The fiscal picture also deserves attention. Interest on the national debt now exceeds $1 trillion annually, and the extension of the 2017 tax cuts adds an estimated $4.6 trillion to deficits over the next decade.[8] That level of structural deficit spending creates pressure on the dollar and on long-term interest rates that will be difficult to fully offset.

There is a version of the current moment that is genuinely worrying: an energy shock that spikes inflation, a Fed that loses credibility during a leadership transition, fiscal deficits that ultimately pressure the dollar and long-term rates, and an AI cycle that peaks before the productivity gains arrive. But there is also a version that looks more like what we’ve seen before: a mid-cycle correction driven by uncertainty, followed by a resolution that allows earnings growth to reassert itself as the dominant driver. History suggests that version is more likely.

The right response to a changed map isn’t to stop moving, but rather to verify that your route still makes sense and adjust where it doesn’t. As always, we’re available to discuss your specific situation if the quarter’s volatility has raised questions about your allocation or your plan.

This commentary is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. The views expressed are those of Brand Asset Management Group as of the date of publication and are subject to change.

[1] Source: Federal Reserve.

[2] Source: J.P. Morgan Asset Management.

[3] Source: FactSet Earnings Insight, April 2, 2026.

[4] Source: CBO.

[5] Source: Morningstar Direct.

[6] Source: Morningstar Direct, performance of the iShares Expanded Tech-Software ETF (IGV).

[7] Source: BlackRock Investment Institute, April 2026.

[8] Source: Bloomberg.