Year of the US Large Cap

4Q 2014

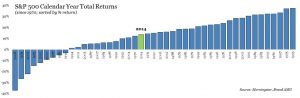

In a year that saw such things as Russian imperialism, the rise of a new terrorist group, fears of an Ebola epidemic, a 46.4% drop in the price of oil, the official end of the Fed’s QE program, and slower economic growth everywhere outside the US, the S&P 500 managed to post another respectable annual return. It finished the year +13.7% (including dividends), near another all-time high (with 53 all-time highs for the year). However, despite its gradual drift higher for most of the year, it wasn’t without its share of bumps in the road. Following a rocky start in January, which had the S&P down 5.8% by February 3rd, the market recovered and spent most of the next seven months grinding higher thanks to some of the strongest economic figures on the planet. Then, in late September it began to top out and move lower in early to-mid October on weaker economic figures – moving it 7.4% lower, before recovering into the end of the year.

Although there wasn’t a significant difference between value and growth factors for large cap stocks (value +13.5% vs. growth +13.1%), it was notable for mid-caps (+14.8% vs. +11.9%, respectively). Mid cap stocks overall performed similarly to large caps (at +13.2%), while small cap stocks were negative for most of the year. However, small caps managed to finish +4.9% for the year after posting an impressive 16.2% gain from their mid-October lows.

In international news, we saw the European Central Bank foreshadow an increased willingness to undertake its own version of QE, the People’s Bank of China cut rates to stimulate demand, and Japan delay their consumption tax hike and offer additional stimulus measures. Despite the fact that many foreign markets were higher in local currency terms on the stimulus news, most currencies depreciated (especially vs a strong US Dollar), which produced negative overall returns for the international indices. The MSCI EAFE (Europe, Asia, Far East index, representing developed markets ex-US) was -4.5% for the year, while the MSCI EAFE small cap index was -4.6%. Emerging markets were down less than their developed markets counterpart, with a full year decline of only -1.8%.

Real Estate was a strong performer within allocations. Global real estate was +14.7%, with the US being the best geography (helped again by a strong dollar), at +28.0%.

In the world of fixed income, contrary to most investors’ expectations for the year, the 10-year Treasury yield actually fell: from 3.04% to 2.17%. And although the benchmark rate declined, not all maturities dropped in yield, resulting in a flattening of the yield curve with 1-3 year yields rising and 5-30 year yields falling. Overall, intermediate bonds (Barclays Aggregate Bond Index) finished +6.0% on the year and short-term bonds (BC Gov’t/Credit 1-5 Year Index) was +1.4%.

Going forward, the market’s biggest (current) concerns continue to be the timing and pace of Fed rate hikes, the duration and impacts of low oil prices, and the ability of foreign authorities to sufficiently resuscitate growth in their respective economies. As always, many other events will likely occur over the course of the next year, surprising investors and providing new reasons to worry. We intend to stay focused on the big picture and do what we do best – providing a steady hand in times of instability and maintaining discipline so that clients can better achieve their financial goals.